One of the services that we offer at Econometría Consultants is projections on principle macroeconomic variables and an analysis of the economic situation in Colombia. This service is offered in conjunction with organizations in twelve Latin American countries which form part of the Latin American Alliance of Economic Consultancies – LAECO.

LAECO presents a monthly summary of the economic and political situation in each country, as well as providing a service of sectoral studies on a local and regional level. The following are a selection of economic analyses carried out by the organization.

January 2025 – Historic minimum wage increase and institutional clash

The government set a 23% increase in the minimum wage for 2026, an unprecedented figure that threatens to push inflation up to 6% and force the Central Bank to raise rates. Faced with the collapse of the tax system, Petro declared an economic emergency to raise taxes, a measure rejected by mayors and governors before the Constitutional Court. At the regional level, Maduro’s removal by the US weakened the official narrative and gave new impetus to the center-right.

December 2025 – Legislative defeats and a divided right wing

Colombia ends the year with a record fiscal deficit of 2.9%, the highest in three decades, driving 3% growth but anchoring inflation at over 5%. In Congress, the government suffered a double blow with the collapse of tax and health reforms, forcing it to cut the 2026 budget. While pension reform remains in the hands of an associate judge, the electoral landscape is fragmented: Paloma Valencia will be the Democratic Center’s candidate, dividing the right wing against De la Espriella.

November 2025 – Consumption at its limit and the end of the ban on polls

GDP grew by a surprising 3.6% in the third quarter, driven by public spending (15%) and consumption, although weak investment (2%) is raising alarms about future growth. Politically, the ruling party flexed its muscles with 2.7 million votes in its primary, consolidating Iván Cepeda as the leader of the left. Following the end of the restrictions imposed by Law 2494, the first polls place Abelardo de la Espriella and Cepeda as the frontrunners, with Sergio Fajardo lagging behind.

October 2025 – Break with the US and fiscal disorder

Bilateral relations with the US collapsed after Trump suspended economic aid and levelled accusations against Petro. Domestically, the 2026 budget is underfunded, while the debate over a minimum wage increase (10-12%) divides the Central Bank. Politically, Daniel Quintero’s withdrawal from the Pacto Histórico consultation highlights fractures within the ruling party, leaving Petro’s electoral strength in a vulnerable position.

September 2025 – US decertification and economic rebound

The economy rebounded in July with growth of 4.1%, although inflation stuck at around 5% and announcements of wage increases for 2026 prevented monetary policy from being loosened. Politically, the government suffered a setback in the Senate with the election of Carlos Camargo to the Constitutional Court, anticipating the collapse of the tax reform. In addition, the US decertified Colombia due to the rise in drug crops, although it granted a waiver to maintain aid on a conditional basis.

August 2025 – Mourning on the right and economic paradoxes

Second quarter GDP (2.1%) disappointed expectations, although durable goods consumption and consumer confidence reached positive levels after five years. Politically, the death of Miguel Uribe Turbay reshaped the opposition, which is now looking for heirs such as Juan Carlos Pinzón or the leader’s own father, Miguel Uribe Londoño. Meanwhile, in the Historic Pact, Petro’s closeness to Daniel Quintero is causing friction with the grassroots, who prefer Gustavo Bolívar.

July 2025 – Dollar is falling while polls are “silenced”

The Colombian peso appreciated to $4,000, driven by the global weakness of the dollar and high local rates, allowing inflation to fall to 4.8% after three years of resistance. Politically, the passage of Law 2494 of 2025 imposes severe restrictions and high costs on public polls, limiting their dissemination until the end of the year. This measure creates information asymmetry and electoral uncertainty, making it difficult to gauge public opinion and for investors to make decisions ahead of 2026.

June 2025 – Atypical growth and streets in the hands of the opposition

The economy surprises with a projected GDP of 3.1% and historic unemployment of 8.8%, although demand keeps inflation stagnant at 5%. While the market already discounts fiscal disorder, the government scores a victory with the resurrection of labor reform, offsetting the slowdown in pension reform. However, the attack on Miguel Uribe Turbay catalyzed a massive opposition march, wresting control of social mobilization from the executive branch ahead of 2026.

May 2025 – Informality on the rise and conflicting narratives

The economy is showing signs of decoupling: while informality is driving employment (759,000 new informal jobs compared to 212,000 formal jobs), tax collection is at risk due to stagnation in key sectors. Politically, Congress’ rejection of the labor reform referendum allows the government to adopt a narrative of “the people against institutions.” Petro is now betting on civil mobilization to regain legitimacy and position his pieces for 2026.

April 2025 – Fiscal crisis and standoff over the referendum

Debt climbed to 60.6% of GDP, requiring an adjustment of $11 trillion that the new minister, Germán Ávila, seeks to cover by raising withholdings and anticipating 2026 revenues, a measure that provides breathing room for the current administration but mortgages the next government. Politically, following the departure of Diego Guevara due to fiscal disagreements, the executive branch submitted the referendum to the Senate, a highly complex technical gamble that seeks to mobilize the left ahead of the 2026 elections.

March 2025 – Fiscal alarm and tension over reforms

Inflation rises to 4.3% driven by tolls and wages, while fiscal credibility plummets after implausible revenue targets are revealed, anticipating non-compliance with the rule in 2025. Politically, the collapse of labor reform fractured the relationship with Congress, leading the government to propose an unfeasible referendum. This maneuver is interpreted as an electoral strategy by the left for 2026 in the face of declining public spending.

February 2025 – Good growth figures but bad news with Trump

In 2024, GDP grew 1.7% with inflation of 5.2%, but fiscal deficit reached 6.8% of GDP and debt reached 60%. The government projects to reduce the deficit to 5.1% in 2025 with a 23% increase in revenues, which is not feasible without reform and spending cuts. On the other hand, tensions with Trump provoked the resignation of Chancellor Murillo. A Council of Ministers evidenced fractures in the government, causing the departure of five ministers and anticipating a recomposition of the left for 2026.

January 2025 – Fiscal problems persist and problems with ELN are added

In 2024, the economy grew to 2%, with inflation at 5.2% and unemployment at 10.2%. For 2025, growth of 2.5%-3% is expected, although risks persist due to diesel prices and devaluation. The fiscal deficit exceeded 5% of GDP, generating a cash crisis. Ceasefire with ELN ended after clashes with FARC dissidents. Trump took office in the US, reconfiguring the bilateral agenda.

December 2024 – Fiscal Crisis and Defeats for the Government

GDP will close 2024 with 1.8% growth, inflation of 5.1% and unemployment of 10.3%. The economy was stronger than expected, but the government faces a fiscal crisis. The finance minister resigned due to scandals, and the financing law failed in Congress. In addition, the political reform was rejected, and the health and justice reforms do not have clear majorities.

November 2024 – Moderate Recovery and Political Risks

The economy shows signs of recovery, with projected growth of 2% in 2024 and 3% in 2025. Inflation declined faster than expected and will close at 5.2%. However, political uncertainty affects markets. The proposal to increase transfers from the General System of Participations generates doubts about fiscal sustainability. Presidential campaign begins.

October 2024 – Economy Resists, but Fiscal Crisis Persists

Inflation dropped to 5.8%, accelerating disinflation without affecting employment, which led the IMF and the World Bank to improve their projections. However, the fiscal deficit remains the biggest risk. In Congress, the labor reform advanced with changes in overtime and parental leave, but generates concern among businessmen for its possible impact on formal employment.

September 2024 – Inflation is decreasing but Foreign Exchange Risks persist

Inflation surprised with 0% monthly, reducing the annual forecast to 5.7%. However, the peso depreciated to 4.200 on US recession fears and domestic fiscal risks. In politics, Congress is debating a budget with a COP 12 trillion deficit, which the government expects to cover with a financing law. Its approval is uncertain due to the weakness of the Finance Minister.

August 2024 – Low Growth and Doubts about the 2025 Budget

GDP grew by only 0.1% in the second quarter, confirming stagnation. The unemployment rate rose to 10.7%, affecting the labor market. In politics, the government presented a budget for 2025 with high spending growth, but without clarity on its financing. The possibility of a new tax reform generates uncertainty in the markets.

July 2024 – Pension Reform and Fiscal Austerity

The government managed to pass the pension reform, but faces lawsuits in the Constitutional Court. The relationship with the Court is tense after several adverse decisions. In the economy, inflation continues at 7%, and the government cut spending by COP 20 trillion to mitigate the deficit, although doubts persist regarding fiscal sustainability. Public debt is growing faster than GDP.

June 2024 – Economic Stagnation and Crisis in Congress

The economy continues to stagnate, with a fall in investment and lower tax collection, aggravating the fiscal deficit. The Constitutional Court blocked key measures to increase revenues. In Congress, the government faces difficulties in passing health and education reforms. Poor implementation of the new health system for teachers generated chaos and protests.

May 2024 – Unemployment on the Rise and Tensions in Congress

Inflation fell to 7.16%, but unemployment rose to 11%, reflecting the effects of tight monetary policy. GDP grew by only 0.9% in the first quarter. In Congress, the pension reform advanced after an agreement that set the threshold at 2.3 minimum wages, but the government tried to increase it to 4.

April 2024 – Health Care Reform Collapse and Fiscal Crisis

Congress shelved the health reform, a key setback for the government. Meanwhile, the Superintendence intervened several EPS, putting at risk the access to health care of millions of affiliates. In the economy, the IMF reduced its growth forecast to 1.1%, and the fiscal deficit increased to 5.3%, threatening the fiscal rule. Inflation continued to decline, reaching 7.3%.

March 2024 – Macroeconomic Risks and Total Peace Crisis

Inflation dropped to 7.7%, but the fiscal deficit and political uncertainty put economic stability at risk. The president proposed a Constituent Assembly, increasing volatility. On the security front, the government suspended the ceasefire with FARC dissidents after an attack on indigenous communities, weakening its Total Peace policy.

February 2024 – Weak Growth and Political Tensions

The Colombian economy grew only 0.6%, well below expectations, reflecting a more turbulent landing. Inflation fell to 8.3%, but unemployment closed the year at 10.8%. In politics, the government faced criticism for errors in the budget decree and generated tensions with the Supreme Court by calling for a march against the attorney general.

January 2024 – Situation Report of the Latin American Alliance of Economic Consultants: 2024, the year of painless disinflation.

2023 was not a good year. The economy will barely grow by 1%, inflation closed at 9.2% and the labour market shows signs of slowing down. The year 2024 is likely to be a year we will remember more fondly. In fact, if things go well, it will be the year in which Colombia will overcome the inflationary outbreak without major social costs.

December 2023 – Situation Report of the Latin American Alliance of Economic Consultants: News about Minimum wage and health reform.

The results of the regional elections are expected to be reflected in the government’s decision on the minimum wage, which, if it ends up being closer to the employers’ demands, would be interpreted as a deradicalization of the government. However, the government is not as weak as it is believed to be since the health care reform managed to pass in Congress and the labor reform has resurfaced.

November 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Government in knock-out after regional elections.

In the last quarter of 2023, a year-on-year growth of -0.3%, consistent with a growth of 1% for the whole year, and confirming the slowdown announced in previous months. On the political front, as polls indicated, there was a “punishment vote” in most of the country’s main departments and provinces. The latter is perceived as a significant blow to the government and the Historical Pact party. The effects of these electoral results have had an impact on the legislature.

October 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Slowdown and inflation strengthen the opposition.

Economic activity data show a significant slowdown, which has been accompanied by a sustained reduction in inflation, which could lead to interest rate cuts. This complex economic scenario strengthens the opposition, who could win in the main cities in the 29 October elections.

September 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Colombia might be reclassified as a frontier market.

As the economy continues to slow, JP Morgan suggests that the Colombian stock market is too small to be considered emerging and could be reclassified as a frontier market. This may be of concern in the medium term. On the political front, the punishment vote remains the baseline scenario for the October elections.

August 2023 – Situation Report of the Latin American Alliance of Economic Consultants: The slowdown weakens the government.

The latest GDP data, presented by DANE confirms the deceleration announced in previous reports. The economy grew by 0.3% annually in the second quarter of 2023 and had a quarter-on-quarter drop of 1%. On the other hand, regional electoral contests have already started, and polls suggest a punishment vote to the government.

July 2023 – Situation Report of the Latin American Alliance of Economic Consultants: The economy is getting colder.

The Colombian economy continues to show signs of cooling. The labor market shows a lower level of employment, which is to be expected after the central bank’s increase in interest rates. The trade balance also shows an improvement, mainly driven by lower imports.

June 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Colombia’s economy is cooling down.

The Colombian economy is finally showing signs of cooling. On the one hand, inflation decreased two months in a row and significantly. Additionally, the unemployment rate increased in April, both due to higher labor participation and lower employment. If this data is indicative of the coming months, it would confirm the entry into the cooling phase of the economy and possibly weak economic activity figures.

May 2023 – Situation Report of the Latin American Alliance of Economic Consultants: The government coalition broke.

In the last month the government had an important change in its cabinet since the departure of

José Antonio Ocampo (Ministry of Finance), Cecilia López (Ministry of Agriculture), and Carolina Corcho (Ministry of Health), among other ministers, and Carolina Corcho (Ministry of Health), among other ministers. In this way, the government cracked the government coalition. Corcho). The replacement of José Antonio Ocampo is Ricardo Bonilla, who retains certain positions of José Antonio Ocampo, and, in others, is even more orthodox than José Antonio Ocampo.

April 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Will interest rates come down soon? No

Colombia is facing a complex stagflation scenario. Inflation rose to 13.3% in March (y-o-y) and shows signs of remaining above double digits at least until the end of the year. Looking at the disaggregated data, we see a slowdown in food inflation. However, the other components continue to rise, which makes it very difficult for Banco de la República to contemplate a decrease in the interest rate.

March 2023 – Situation Report of the Latin American Alliance of Economic Consultants: Is the next global recession comming?

The first warning sign was the failure of Silicon Valley Bank. Although this bank is not systemic, it is of great importance for the technology and startup sector and can generate contagion effects. Such contagion effects have been seen at Credit Suisse Bank, which is systemic. Thus, the potential failure of Credit Suisse could be the beginning of a new Lehman Brothers, which was the catalyst for the 2008 crisis.

February 2023 – Situation Report of the Latin American Alliance of Economic Consultants: The slowdown has already begun.

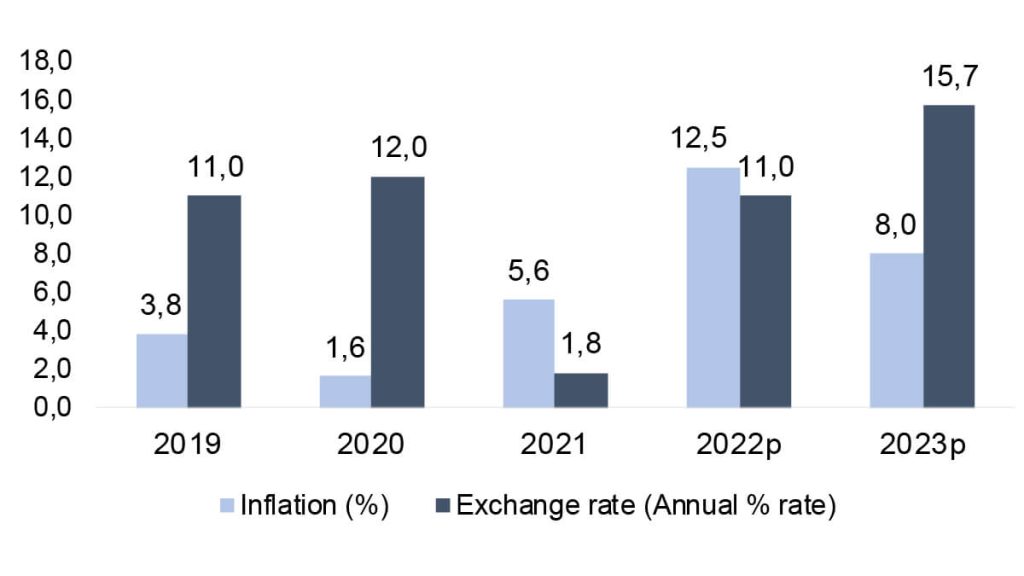

In 2022, the Colombian economy grew by 7.5%. Although the number is high compared to the region, it compares negatively to the market’s expectation (8%), which is similar to Econometría’s expectation. Thus, this suggests the beginning of the economic slowdown. Therefore, the 2023 growth forecast is updated to 0.5% with a downward bias. Regarding inflation, the year-end inflation forecast is increased to 9%.

January 2023 – Situation Report of the Latin American Alliance of Economic Consultants: 2023: Less GDP growth and higher inflation.

2023 starts with downward updates on several indicators. Monetary policy is already significantly affecting household consumption. As far as inflation is concerned, we have no major change in our expectation. We continue to see inflation closing 2023 at 7 to 8%. However, there are some upside risks from the exchange rate.

December 2022 – Situation Report of the Latin American Alliance of Economic Consultants: 2022 is cooling off.

While 2022 will close with 12.7% inflation and possibly grow between 8 and 8.5%, 2023 will be a complex year. On the one hand, the effects of the Banco de la Republica’s monetary policy are already cooling household consumption, which dropped 2.2% in the third quarter of 2022, which is similar to the drop seen in the last quarter of 1998 (2.4%), marking the beginning of the crisis at the end of the century. The growth forecast for 2023 is 2% with downward risks.

November 2022 – Situation Report of the Latin American Alliance of Economic Consultants: Fiscal and trade deficits are at unsustainable levels.

Fundamental variables such as Colombia’s current account deficit and fiscal deficit are at unsustainable levels, making Colombia more vulnerable to the actions of the Federal Reserve. As a result, Colombia is one of the countries with the highest devaluation associated with interest rate increases in the United States. To this cocktail is added the timidity of the Central Bank in raising interest rates. The political situation in Colombia generates even more uncertainty.

October 2022 – Situation Report of the Latin American Alliance of Economic Consultants: A black cloud is rising in the sky, a strong storm is coming.

Although 2022 seems to be a good year in terms of growth, with the latest available information it is credible that Colombia will have a growth between 8-8.5% in 2022, this indicator has as a counterpart an inflation between 12-13%. The monetary tightening that the different central banks are doing will surely make financial conditions tighter and generate a complex 2023.

September 2022 – Situation Report of the Latin American Alliance of Economic Consultants: The temperature rises and rises, the temperature rises.

Even though Banco de la República has raised the monetary policy rate to 9%, it does not appear that the real economy is slowing down. On the contrary, the economy continues to outperform market growth expectations. The dollar has continued its devaluation and is hovering around 4400 COP/USD.

On the political front, Gustavo Petro’s government faced its first march. It was an event without disturbances and not very cohesive, but larger than expected.

August 2022 – Situation Report of the Latin American Alliance of Economic Consultants: The recently elected government begins with a tax reform proposal.

In Colombia, the first presidential term of the left has just begun. This has generated expectations among investors and uncertainty about what will happen in the next 4 years. The government has also shown economic orthodoxy by presenting a tax reform in order to increase revenue. While this tax reform has a high component on personal income and the elimination of exemptions for certain business sectors that is unattractive to investors, such an effort suggests the priority of closing the fiscal deficit generated by the COVID-19 crisis and the search for responsible financing of public spending in the following years.

July 2022 – Situation Report of the Latin American Alliance of Economic Consultants: The world in recession, Colombia overheated

The last few weeks have been characterized by high uncertainty. On the one hand, countries such as the United States and Japan show signs of recession. The greater global risk generates a greater flow of capital towards safer assets than the Colombian currency, such as the dollar and gold, devaluing our currency. Additionally, the election of President Gustavo Petro (leftist candidate) has had an impact on a greater perception of country risk, fueling the devaluation and increases in TES yields and falls in Ecopetrol shares.

June 2022 – Situation Report of the Latin American Alliance of Economic Consultants: A step to the left.

On June 19, Colombians elected Gustavo Petro as their president for 2022-2026. This is a relevant change for the country. First, he is the first leftist president who generates uncertainty. However, moderation of his policies is expected since he does not have majorities in Congress, and he made many alliances with the political center during his campaign.

On the other hand, the economy has shown important signs of recovery, which is why the growth forecast is updated to 8.5% for 2022.

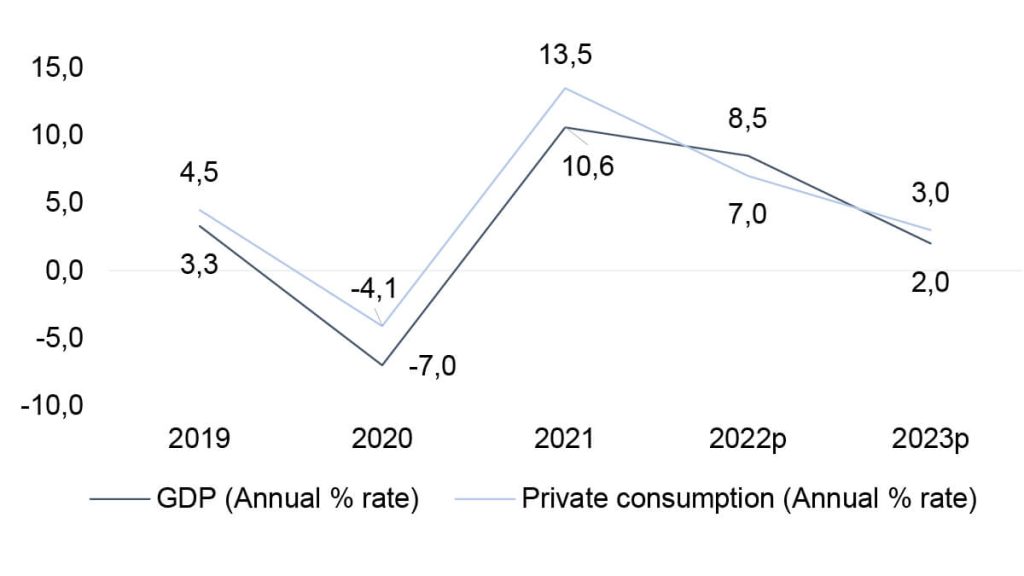

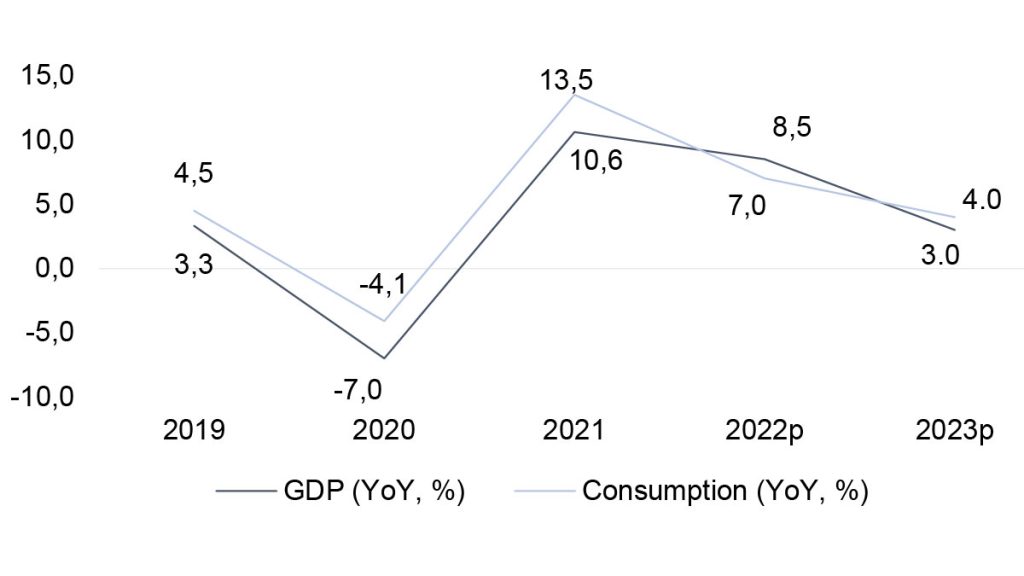

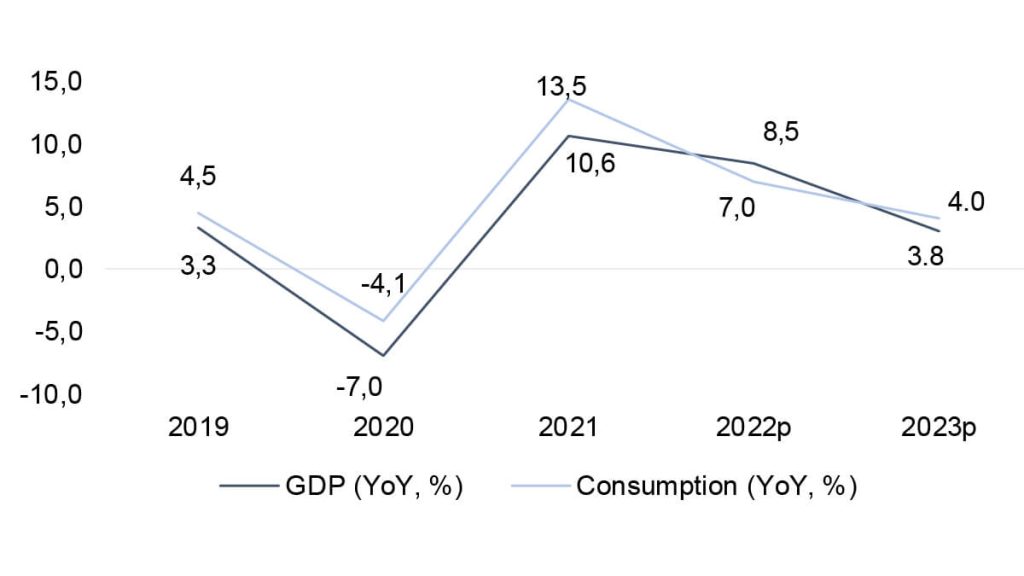

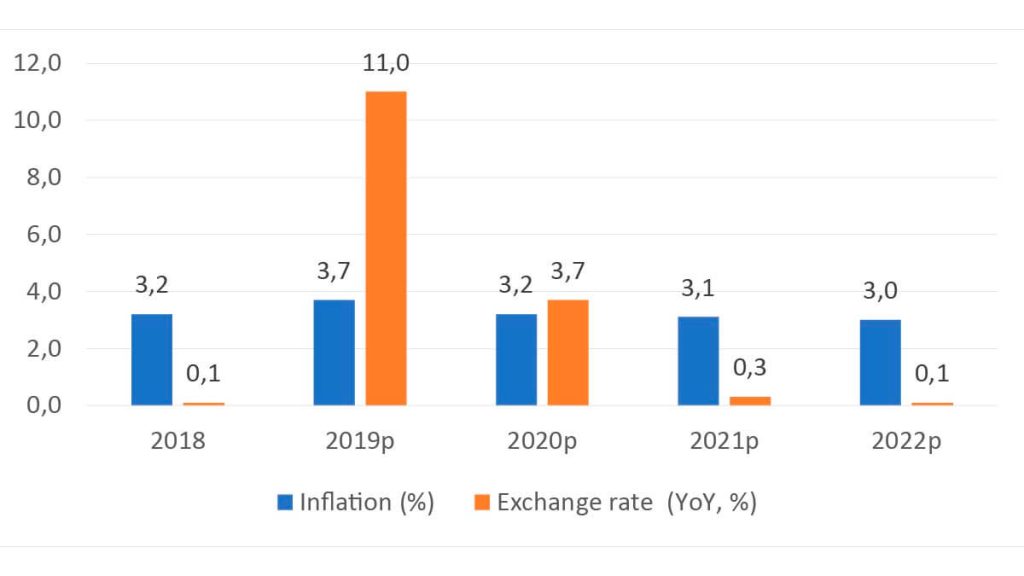

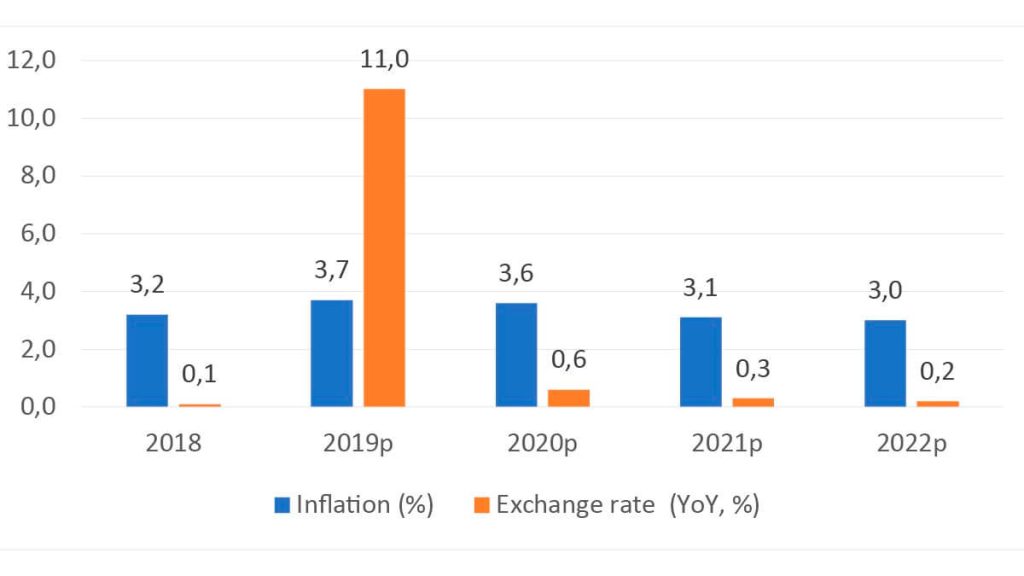

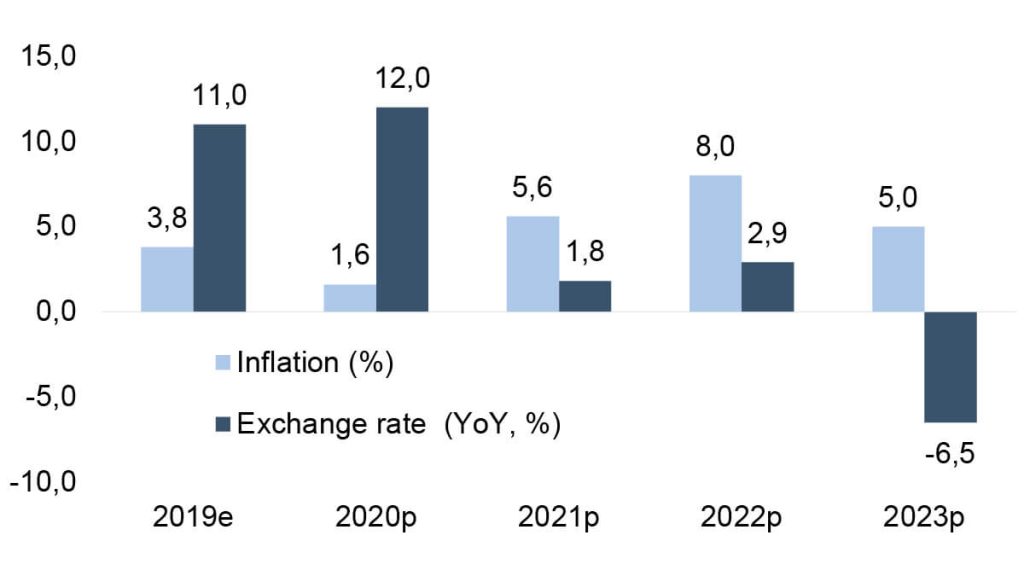

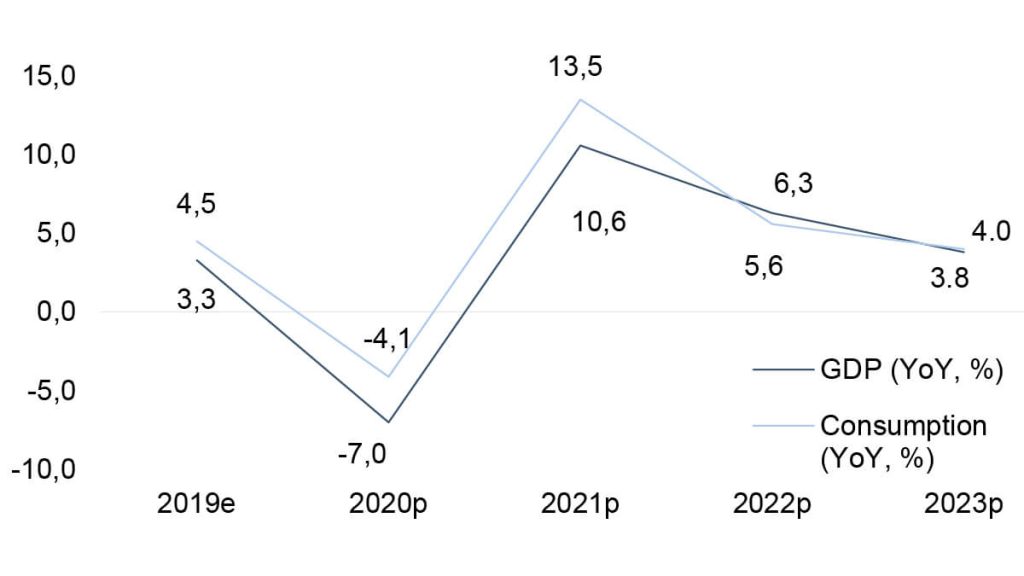

December 2019 – The Colombian economy

Although the Colombian economy continues to show high growth compared to other economies in the region, it has imbalances in the fiscal and current account deficits that make it unlikely that it will increase public spending. On the other hand, in monetary policy there is also no room to apply expansionary policies, since inflation would close the year close to the target range (3.9%). Econometrics Consultants reduces the forecast for economic growth from 3.2% to 3.1% in 2019 and increases the forecast for the unemployment rate from 10.6% to 10.8%.

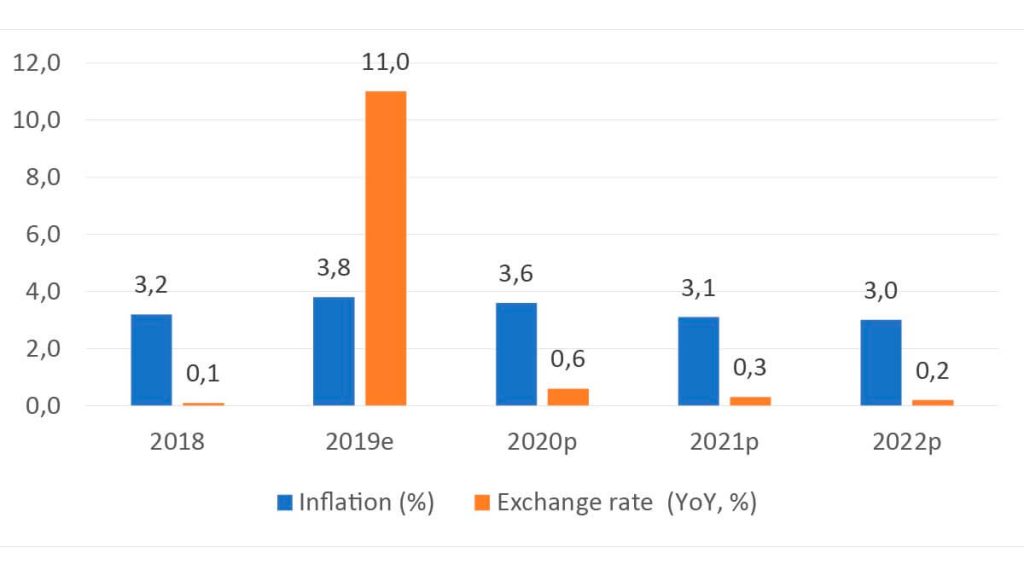

January 2020 – Factors that could slow down the growth of the world economy

The Colombian economy will end 2019 with economic growth close to 3.1%. Inflation closed at 3.8% and it is estimated that the unemployment rate was above 10%. In this context, the projections of Econometrics Consultants for 2020 are similar. In particular, global demand will have a slight boost in 2020, but factors such as Brexit, the conflict between the United States and Iran, the impeachment of Donald Trump, among others, could slow down the growth of the world economy.

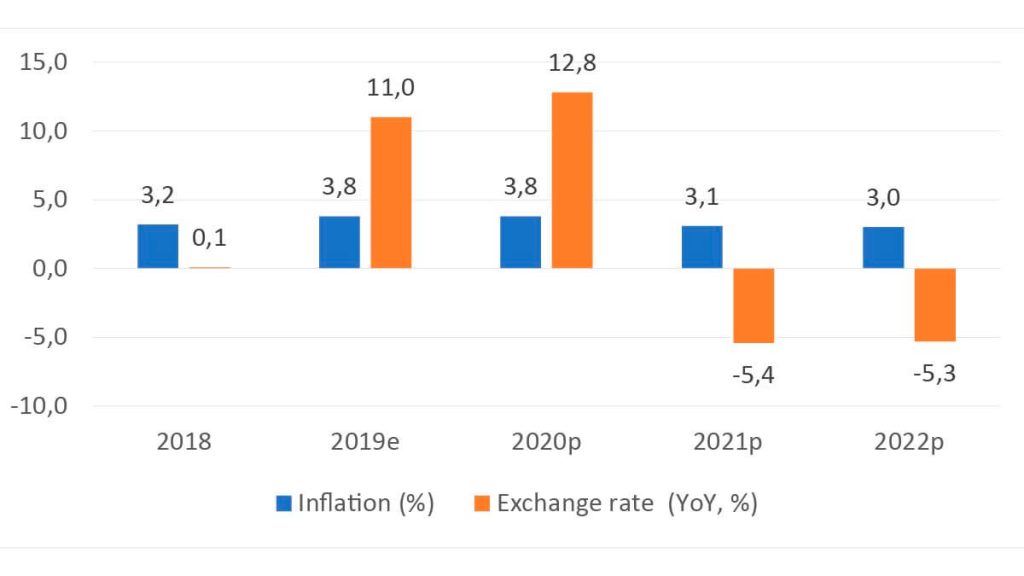

February 2020 – The volatility of the markets continues due to the coronavirus

Although the uncertainty generated by Brexit and the impeachment of Donald Trump has ceased, the volatility of the markets continues thanks to the coronavirus, devaluing the Colombian currency. In this way, if this trend continues, our central scenario of an average exchange rate around 3,300 COP/USD during 2020 could be modified. On the other hand, there are reasons for relief in the Colombian economy as inflation slowed to 3.6% (year-on-year) and growth in 2019 was 3.3%.

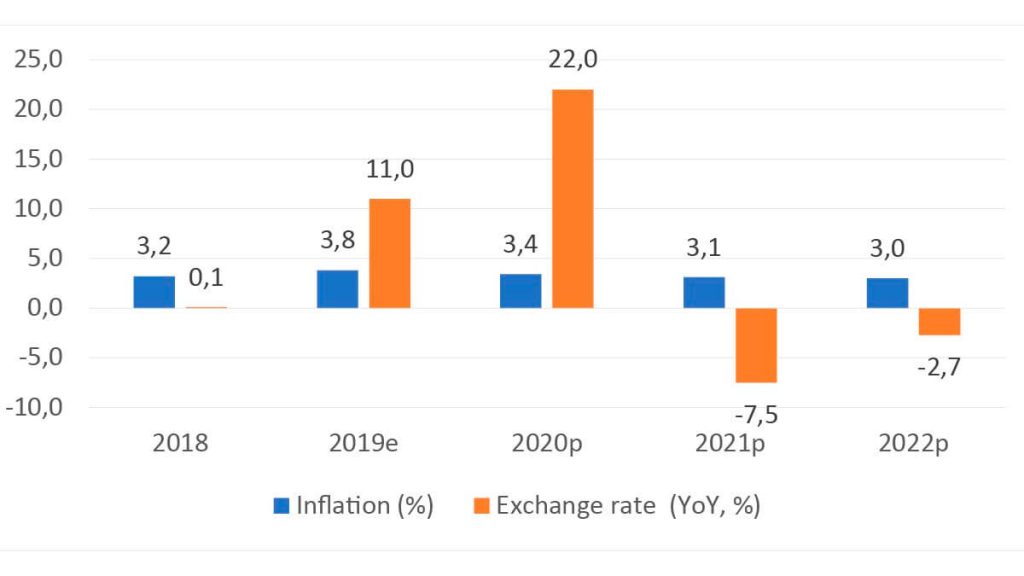

March 2020 - Fall in oil prices and the global effects of the Coronavirus

Colombia has been affected by the drop in oil prices and the global effects of the Coronavirus on demand, which has affected the trade balance, the fiscal balance, the exchange rate and inflation. At the moment, the forecasts of the previous month are maintained because there have not yet been any signs that suggest that the epidemiological situation in Colombia is difficult to manage and quarantines are required.

April 2020 - COVID-2019 LAECO special report

The Latin American Alliance of Economic Consultants – LAECO, presents a special report on the situation of COVID-19 in Latin America and the responses that governments have given to face the crisis.

May 2020 - Report of the Latin American Alliance of Economic Consultants: Projections of the effect of the COVID-19 crisis on the economies

The LAECO Alliance publishes its forecasts for growth, inflation, unemployment and other macroeconomic variables of the Latin American economies for the month of May 2020. A significant contraction is forecast in all countries due to the crisis generated by COVID- 19, which in some economies is accentuated by the decrease in oil prices and other commodities. For the Colombian case, Econometrics Consultants forecasts a GDP variation of -3.0% for this year. To obtain more information about this analysis, request your subscription to the LAECO Monthly Bulletin.

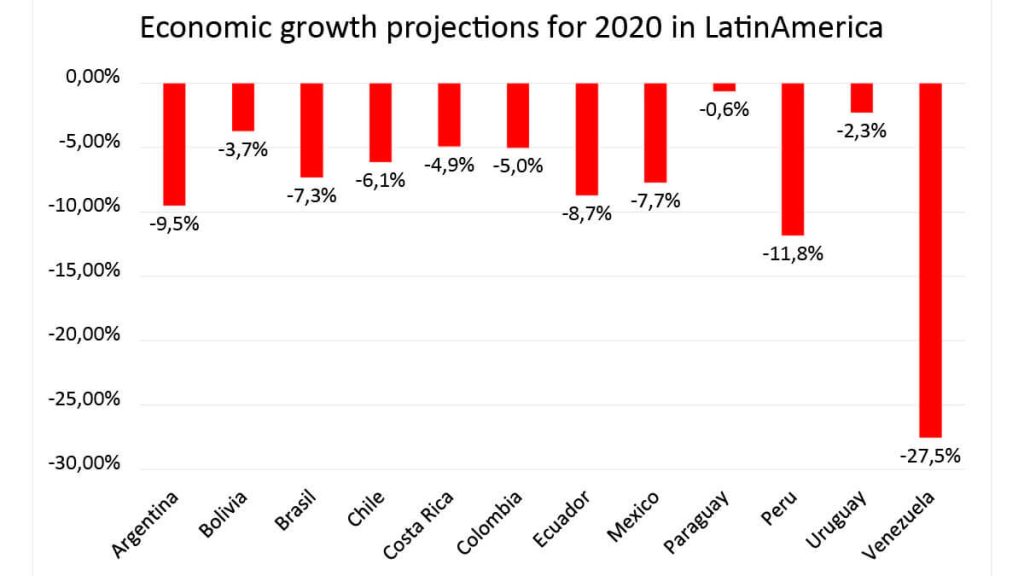

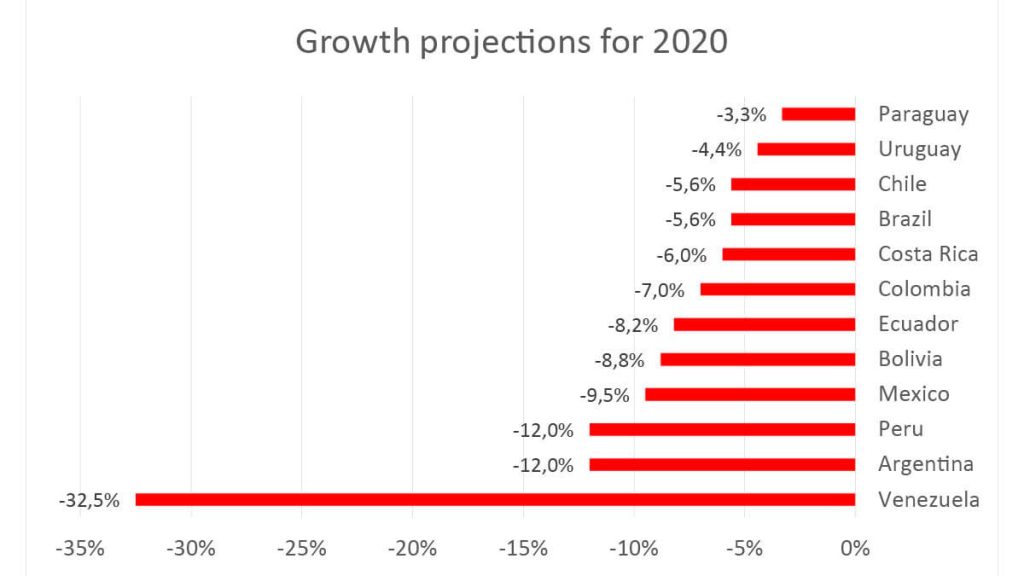

June 2020 – Report of the Latin American Alliance of Economic Consultancies LAECO: Growth projections for 2020

The LAECO Alliance adjusts its forecasts for growth, inflation, unemployment and other macroeconomic variables of the Latin American economies for 2020. A sharp drop in the economic growth of the countries is expected, which varies between -0, 6% forecast for Paraguay, and -27.5% forecast for Venezuela.

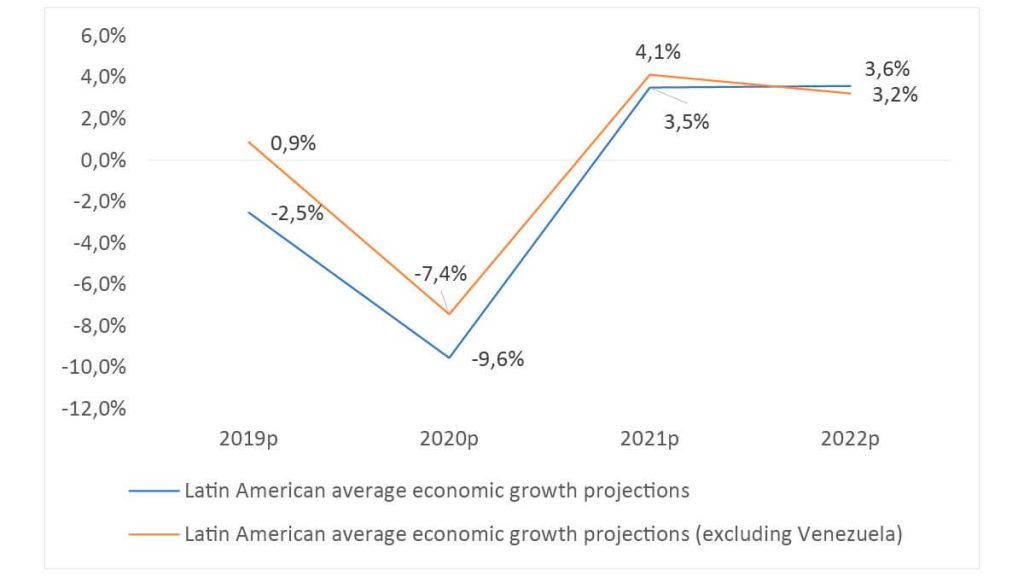

July 2020 - Report of the Latin American Alliance of Economic Consultancies LAECO: Growth recovery for 2021

According to the LAECO Alliance countries, the average of the growth forecasts in Latin America in 2020 is -9.6%, and -7.4% excluding Venezuela. The economies are expected to recover in 2021, forecasting an average growth for that year of 3.5% and 4.1% excluding Venezuela.

August 2020 - Report of the Latin American Alliance of Economic Consultants: Colombia slightly above the average for Latin America

The economic growth forecasts of the LAECO Alliance countries project an expected growth of -9.14% for the countries of the region in 2020. Colombia is slightly above this average, with a forecast of -7%.

September 2020 - Situation Report of the Latin American Alliance of Economic Consultants: Prices going down

The countries of the LAECO Alliance project an average inflation of 1.40% for 2020, a figure lower than the 2.58% presented in 2019. The COVID-19 crisis will also be reflected in prices, although the figures are expected to increase again from 2021.

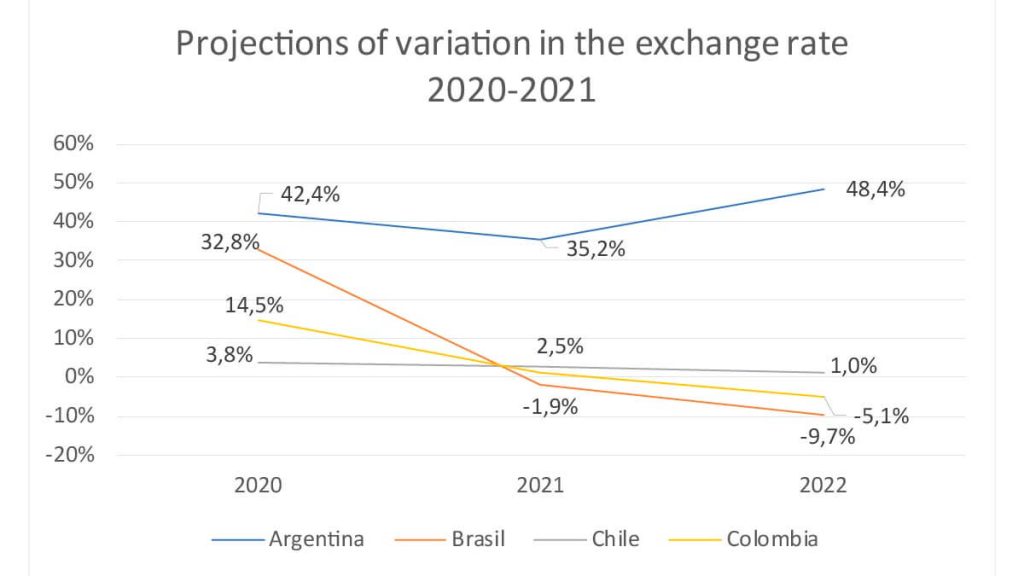

October 2020 - Situation Report of the Latin American Alliance of Economic Consultants: Lower devaluation

The LAECO Alliance countries project a lower devaluation of their currencies for 2021, compared to the one presented in 2020. This trend is expected to continue in 2022 in most countries, except for Argentina where an increase in devaluation is forecast for the Argentinean Peso in that year.

November 2020 - Situation Report of the Latin American Alliance of Economic Consultants: Expected growth of -9.6% for the region

The LAECO Alliance countries project, on average, a 9.6% production contraction for 2020. The biggest drop is expected in Venezuela, Argentina and Peru, while the most optimistic forecasts are in Paraguay and Uruguay.

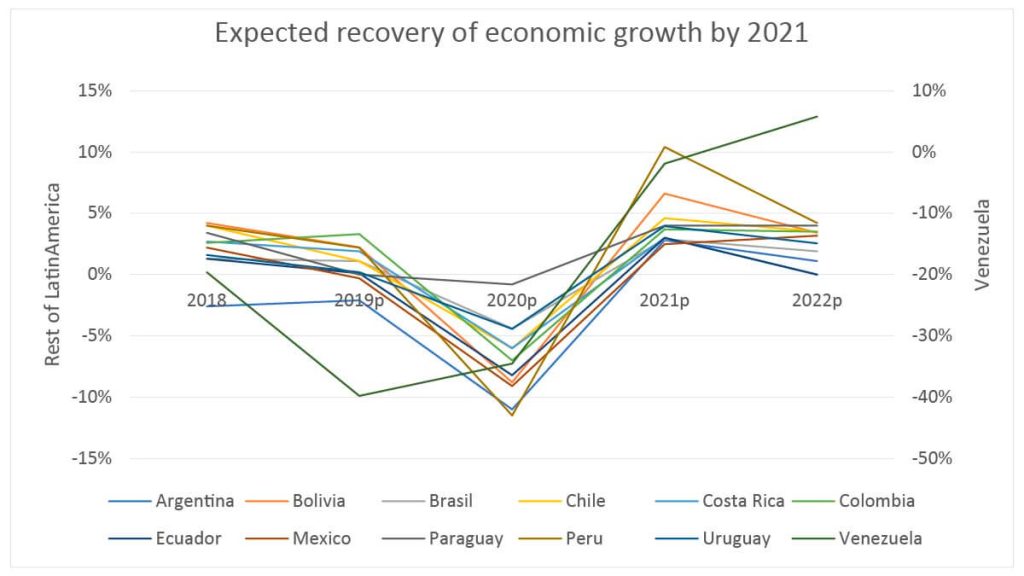

December 2020 - Situation Report of the Latin American Alliance of Economic Consultants: V recovery expected by 2021

The countries of the LAECO Alliance project an economic growth recovery of the region in a V-shape, since the -9.31% expected in 2020, it expected to be replaced by a positive 3.8% in 2021. If these projections are met, all Latin American countries would present growth of more than 2.5% next year, with the exception of Venezuela where, although growth is expected to be negative, an economic recovery is foreseen.

January 2021 - Situation Report of the Latin American Alliance of Economic Consultants: What is expected for the exchange rate of Latin American currencies in 2021?

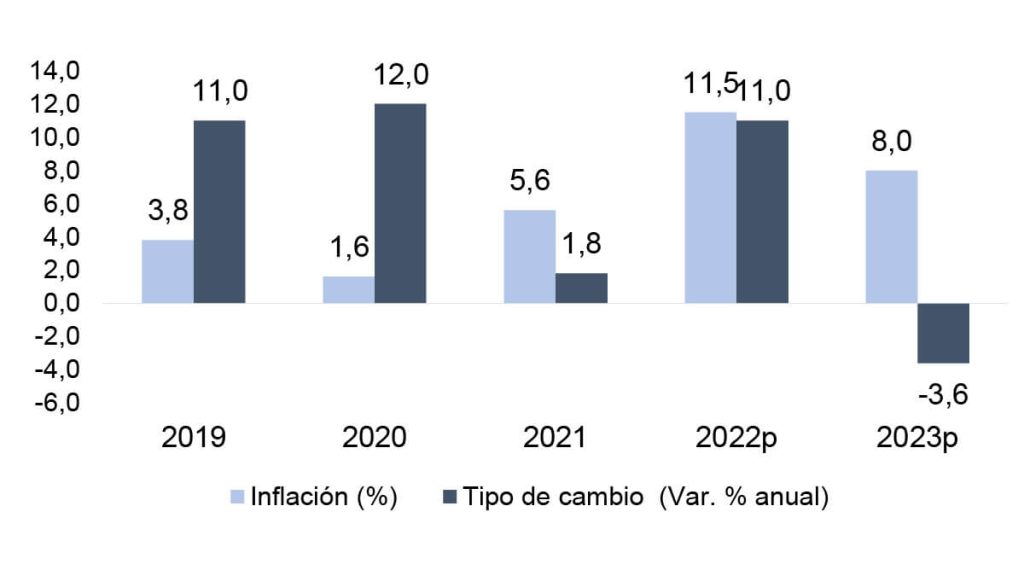

The LAECO Alliance countries estimate a devaluation of their currencies with respect to the US dollar of 6.83% on average during 2021. However, estimates vary. While in countries such as Argentina devaluations close to 50% are expected, in Colombia a revaluation of 12% of the Colombian peso is estimated compared to the exchange rate values presented in 2020.

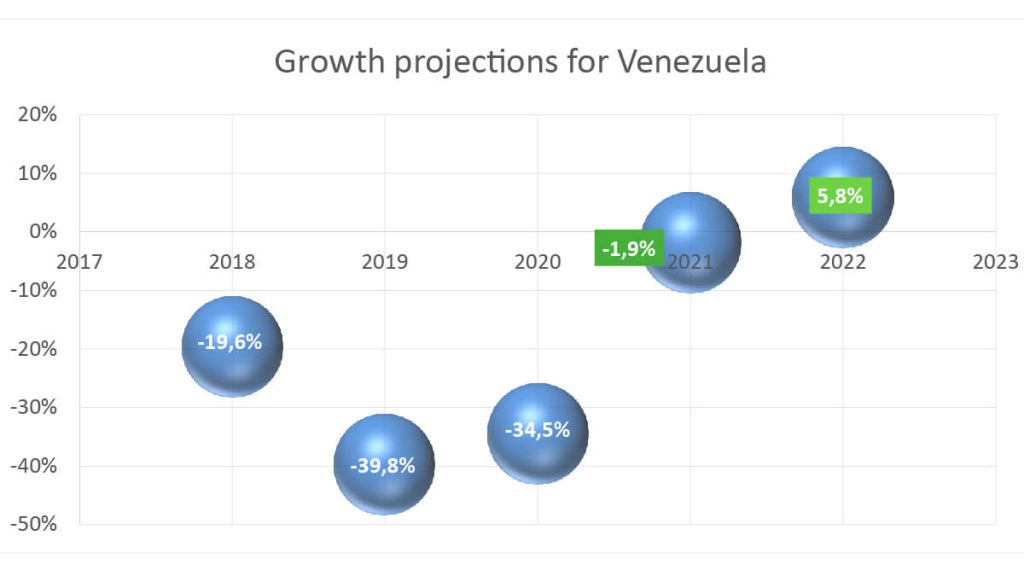

February 2021 – Situation Report of the Latin American Alliance of Economic Consultants: What are the growth expectations in Venezuela this year?

Ecoanalítica, a member of the LAECO Alliance, estimates a decrease of -1,9% of the Venezuelan economy for 2021 and an increase of 5.8% for 2022. These are positive expectations, considering the GDP contraction of 39.8 % and 34.5% presented in 2019 and 2020 respectively.

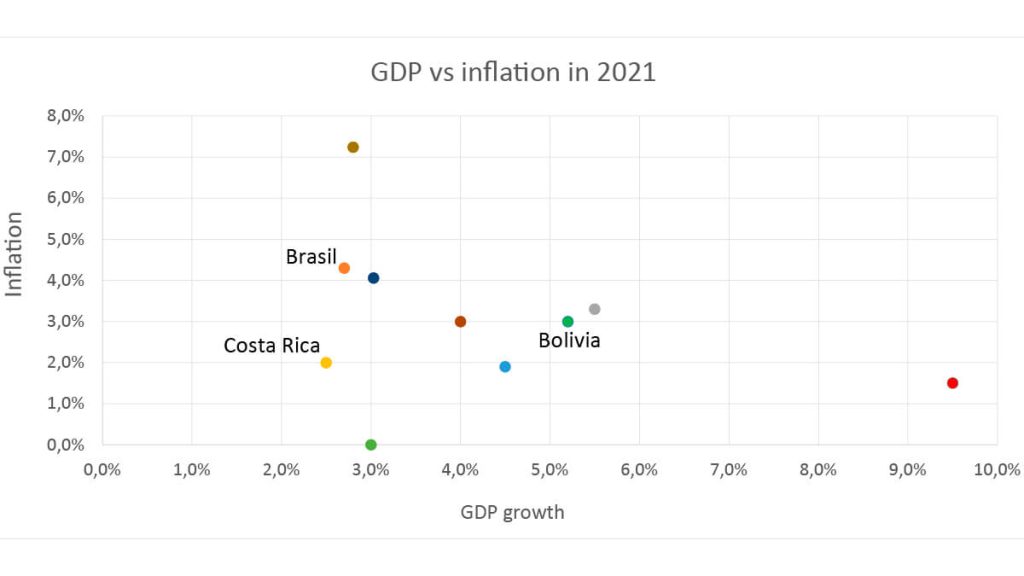

March 2021 – Situation Report of the Latin American Alliance of Economic Consultants: Will GDP grow more than inflation in Latin America in 2021?

Most of the countries of the LAECO Alliance estimate similar levels of GDP growth and inflation in 2021. In countries such as Uruguay, inflation is estimated to be much higher than economic growth, while in Peru the relationship is inverse.

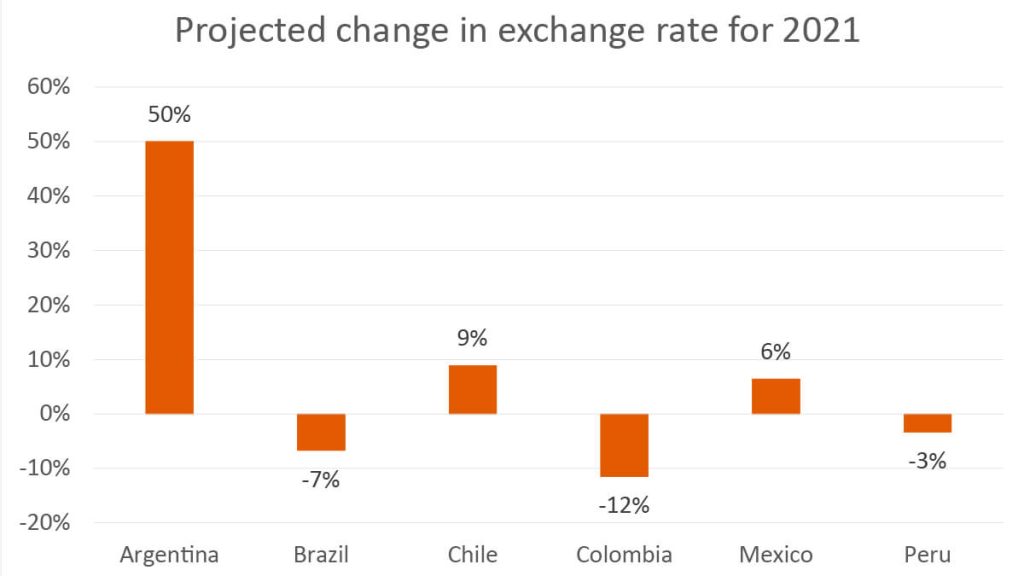

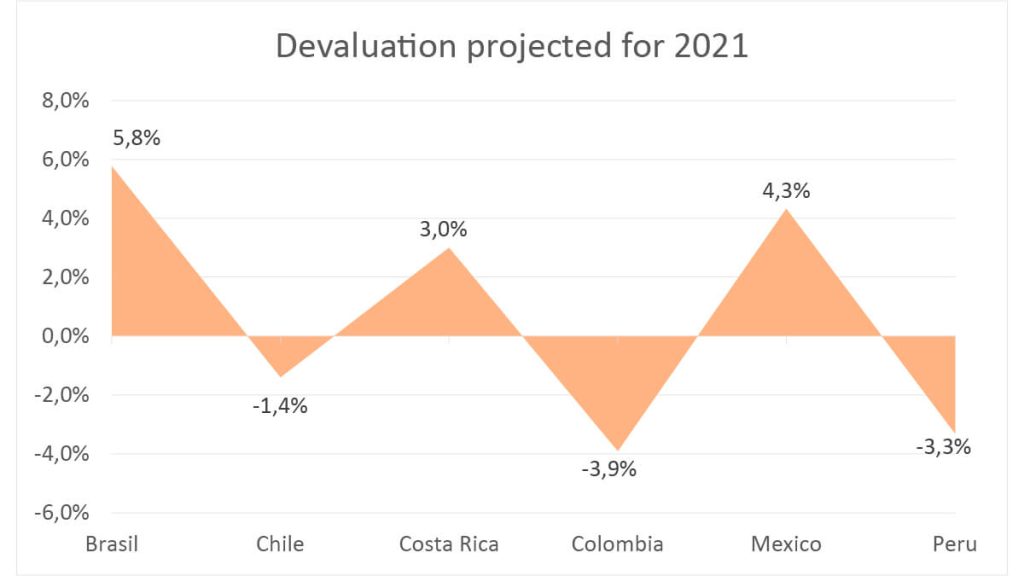

April 2021 – Situation Report of the Latin American Alliance of Economic Consultants: Devaluation and revaluation expected for 2021

The exchange rate projections for 2021 of the LAECO Alliance countries are diverse, varying in estimates of revaluation of the Chilean peso, the Colombian peso and the Peruvian sol, to estimates of devaluation in other currencies such as the Brazilian real, the Mexican peso and the Costa Rican colon.

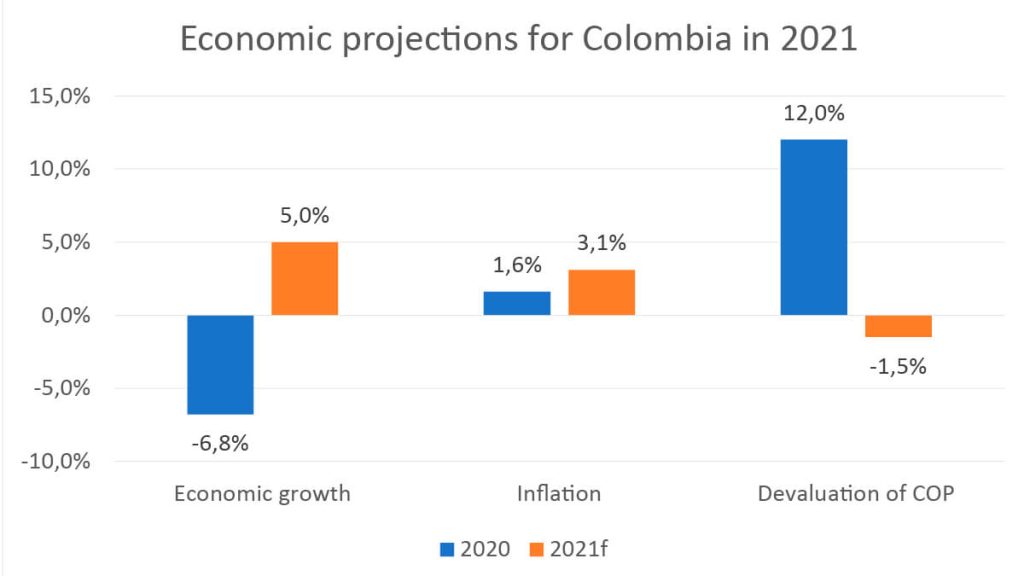

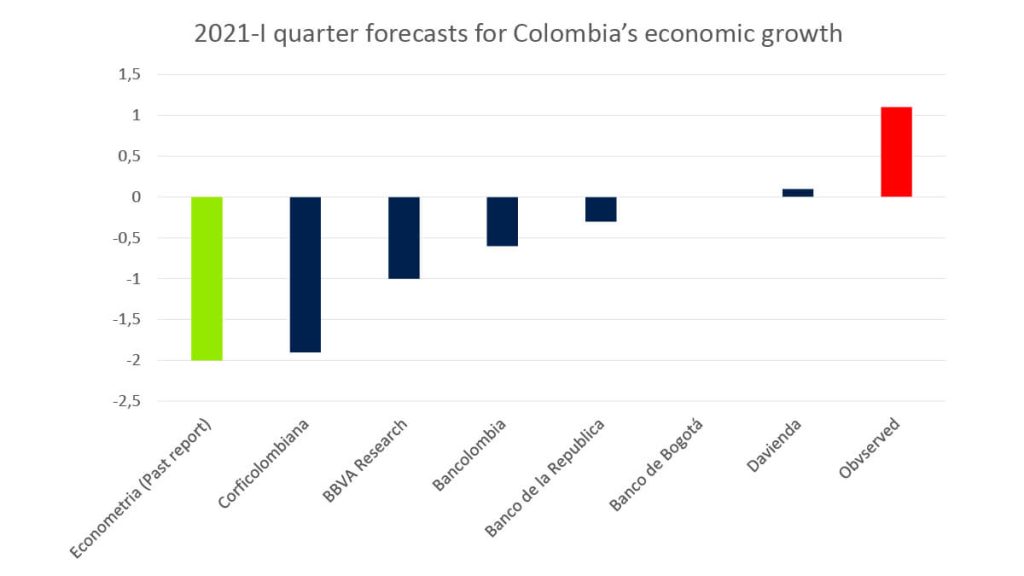

May 2021 – Situation Report of the Latin American Alliance of Economic Consultants: Positive forecasts for Colombia in 2021

Despite the economic and political shocks presented in the first quarter of the year, an improvement in the economic growth of the Colombian economy is expected for 2021 and a lower devaluation of the peso compared to 2020. However, this behavior will be accompanied by an increase in inflation.

June 2021 - Situation Report of the Latin American Alliance of Economic Consultants: Positive forecasts for Colombia in 2021

The Colombian economy recovered in the first quarter of the year, contradicting forecasts from different economic analysts. Considering this positive trend, Econometría Consultores has adjusted its economic growth projection to levels over 6% by the end of this year.

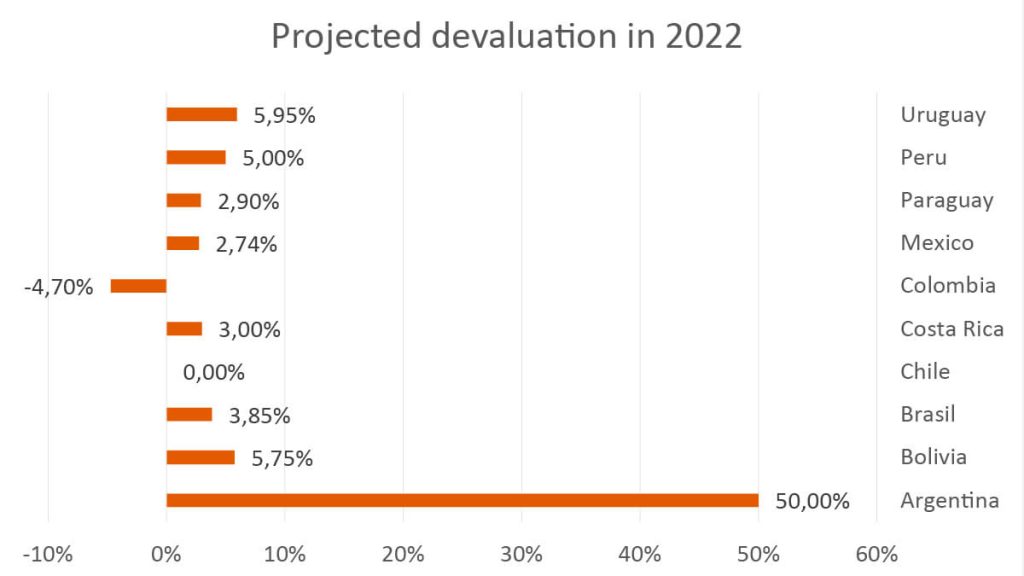

July 2021 - Situation Report of the Latin American Alliance of Economic Consultants: Devaluation expectations for 2022

In most Latin American countries, a reduction in the value of the local currency is expected by 2022, except for Colombia and Chile, where a lower devaluation is projected next year.

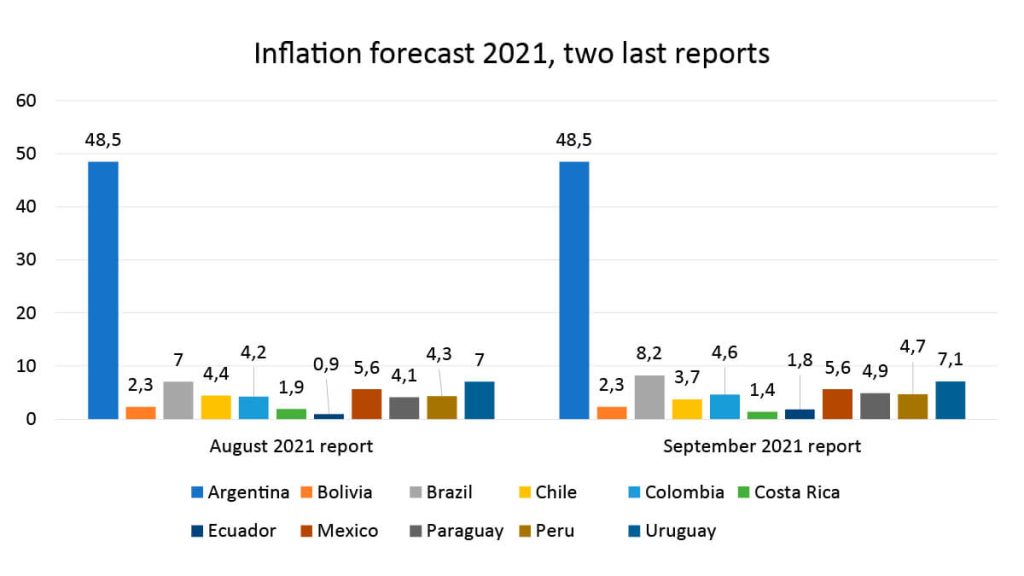

September 2021 – Situation report of the Latin American Alliance of Economic Consultants: Inflation projections for 2021

In most Latin American countries, 2021 inflation forecasts have been updated upwards due to exchange rate pressures and a rise on food inflation.

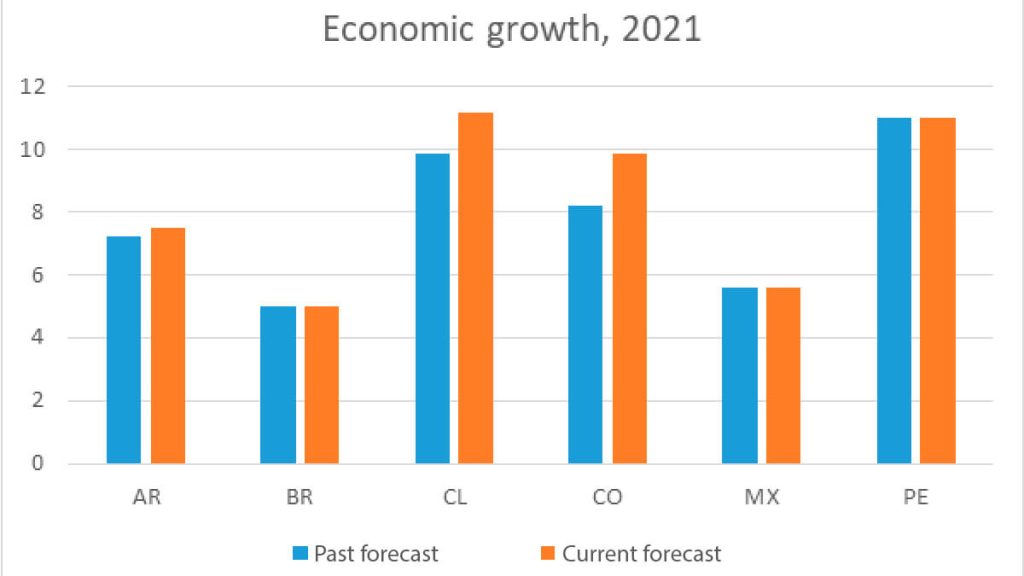

October 2021 – Situation report of the Latin American Alliance of Economic Consultants: Better growth expectations in the region

Our current forecasts in LAECO for GDP growth in the main economies of the region in 2021 (in parentheses the forecast in September): AR 7.5 (7.2) BR 5.0 (5.0) CL 11.2 (9.9) CO 9.9 (8.2) MX 5.6 (5.6) EP 11 (11)

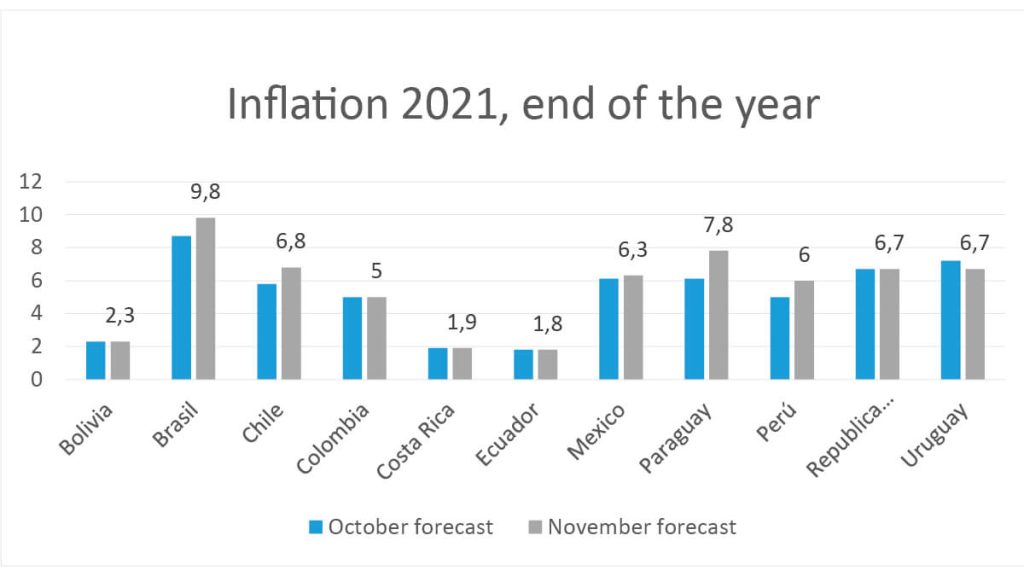

November 2021 – Situation report of the Latin American Alliance of Economic Consultants: Inflation on the rise

Just as in past months, growth forecasts for 2021 were increased for most countries in the region. Inflation forecasts have also increased for both 2021 and 2022. This is due to supply chain bottlenecks, a steeper devaluation and a pick-up in economic growth.

December 2021 – Situation report of the Latin American Alliance of Economic Consultants: A good 2021 and a challenging 2021

The Colombian economy will end 2021 with a good performance and 2022 will be a good year, although there are relevant risks. Inflation continues to rise and will generate further interest rate increases. The unemployment rate remains above the pre-pandemic level. Despite this, the economy is expected to grow by about 5% in 2022.

January 2022 – Situation report of the Latin American Alliance of Economic Consultants: Inflation and political uncertainty

2021 inflation reached 5.6%, well above the inflation target, which will force Banco de la República to raise the monetary policy interest rate.The political context is uncertain and Colombia faces risks of extremes like in Chile and Perú that could harm the future of the economy.

February 2022 – Situation report of the Latin American Alliance of Economic Consultants: Base effects growth

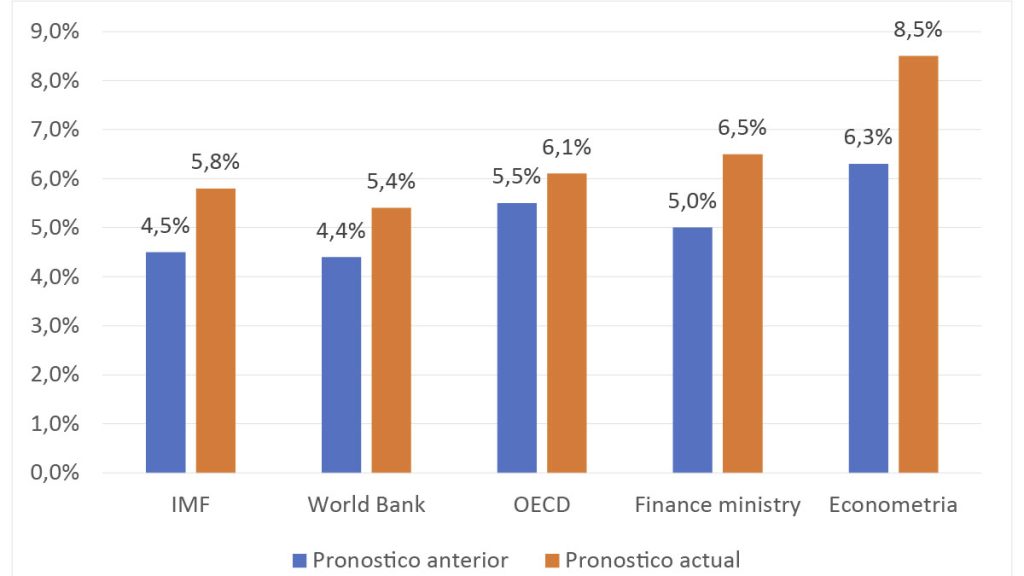

DANE revealed that 2021 GDP growth was 10.6%. If the economy stagnates at 2021Q4 GDP levels for all 2022, 2022 GDP growth would be around 5.3%. Thus, we updated our GDP growth forecast to 6.3%, which is similar to a 3% GDP in normal times. This growth rate might be insufficient for job creation.

March 2022 – Situation report of the Latin American Alliance of Economic Consultants: When it rains, it pours

Russia’s invasion of Ukraine will put further pressure on food and energy prices, as both countries are major exporters of corn, wheat and fertilisers such as urea, and in the case of Russia, blockades on its oil exports increase oil prices.

In Colombia, electoral uncertainty is increasingly relevant as left-wing options seem to be gaining strength. For the moment, congressional and senate elections suggest that no party will have majorities without alliances. However, the results of the new count are awaited.

April 2022 – Situation report of the Latin American Alliance of Economic Consultants: An overheated economy?

As predicted in previous months, inflation has continued to rise. As of March, monthly inflation was 1%, and annual inflation reached 8.5%. In response, Banco de la República raised its benchmark interest rate by 100 basis points at its March meeting. On the positive side, the labor market is recovering.

Marisol Rodríguez es ingeniera de sistemas con especialización en gerencia de proyectos de la Universidad Autónoma de Colombia y magíster en Política Social de la Universidad Javeriana. Se encuentra vinculada a Econometría desde el año 2001, participando en algunos proyectos realizados por la firma y en los últimos años como gerente del área de licitaciones. Sus áreas de interés son las políticas públicas con especial énfasis en los sectores de protección social y educación. Cuenta con amplia experiencia en el sistema de compras públicas del Estado colombiano, así como de organismos internaciones y la banca multilateral.

Marisol Rodríguez

Gerente de Propuestas

Marisol Rodríguez es ingeniera de sistemas con especialización en gerencia de proyectos de la Universidad Autónoma de Colombia y magíster en Política Social de la Universidad Javeriana. Se encuentra vinculada a Econometría desde el año 2001, participando en algunos proyectos realizados por la firma y en los últimos años como gerente del área de licitaciones. Sus áreas de interés son las políticas públicas con especial énfasis en los sectores de protección social y educación. Cuenta con amplia experiencia en el sistema de compras públicas del Estado colombiano, así como de organismos internaciones y la banca multilateral.

Hernán Herrera

Consultor de Proyectos

Hernán Herrera es estadístico y magíster en Estadística Aplicada, con más de 10 años de experiencia en analítica, modelamiento estadístico y automatización de procesos de datos. Actualmente se encuentra vinculado a Econometría desde hace dos años, participando en proyectos enfocados en muestreo probabilístico, estimación con factores de expansión, ajuste por no respuesta y control de calidad en operativos de campo. Cuenta con experiencia en sector público y privado, así como en el uso de herramientas como R, Python, SQL y Power BI para la generación de insumos técnicos orientados a la toma de decisiones.

Hernán Herrera

Consultor de Proyectos

Hernán Herrera es estadístico y magíster en Estadística Aplicada, con más de 10 años de experiencia en analítica, modelamiento estadístico y automatización de procesos de datos. Actualmente se encuentra vinculado a Econometría desde hace dos años, participando en proyectos enfocados en muestreo probabilístico, estimación con factores de expansión, ajuste por no respuesta y control de calidad en operativos de campo. Cuenta con experiencia en sector público y privado, así como en el uso de herramientas como R, Python, SQL y Power BI para la generación de insumos técnicos orientados a la toma de decisiones.

Hernán Herrera

Project Consultant

Hernán Herrera is a statistician with a Master’s degree in Applied Statistics, with more than 10 years of experience in analytics, statistical modeling, and data process automation. He is currently working at Econometría, where he has been for the past two years, participating in projects focused on probabilistic sampling, estimation using expansion factors, nonresponse adjustment, and quality control in field operations. He has experience in both the public and private sectors, as well as in the use of tools such as R, Python, SQL, and Power BI for generating technical inputs to support decision-making.

Hernán Herrera

Project Consultant

Hernán Herrera is a statistician with a Master’s degree in Applied Statistics, with more than 10 years of experience in analytics, statistical modeling, and data process automation. He is currently working at Econometría, where he has been for the past two years, participating in projects focused on probabilistic sampling, estimation using expansion factors, nonresponse adjustment, and quality control in field operations. He has experience in both the public and private sectors, as well as in the use of tools such as R, Python, SQL, and Power BI for generating technical inputs to support decision-making.

Gabriel Hernández

Consultor de Proyectos

Gabriel Alejandro Hernández Muñoz es politólogo. Cuenta con experiencia laboral en la evaluación de proyectos de inversión, programas y políticas públicas desde enfoques, metodologías y técnicas cualitativas; también ha ahondado en temas relacionados con construcción de paz desde enfoques de lucha contra la corrupción, acceso a la información y transparencia. Está vinculado con Econometría desde el 2024 como analista cualitativo, encargándose del desarrollo de metodologías de investigación, sistematización y análisis de información cualitativa.

Gabriel Hernández

Consultor de Proyectos

Gabriel Alejandro Hernández Muñoz es politólogo. Cuenta con experiencia laboral en la evaluación de proyectos de inversión, programas y políticas públicas desde enfoques, metodologías y técnicas cualitativas; también ha ahondado en temas relacionados con construcción de paz desde enfoques de lucha contra la corrupción, acceso a la información y transparencia. Está vinculado con Econometría desde el 2024 como analista cualitativo, encargándose del desarrollo de metodologías de investigación, sistematización y análisis de información cualitativa.

Gabriel Hernández

Project Consultant

Gabriel Alejandro Hernández Muñoz is a political scientist with professional experience in evaluating investment projects, programs, and public policies using qualitative approaches, methodologies, and techniques. He has also delved into topics related to peacebuilding from the perspectives of anti-corruption, access to information, and transparency. He has been with Econometría since 2024 as a qualitative analyst, where he is responsible for developing research methodologies, as well as systematizing and analyzing qualitative data.

Gabriel Hernández

Project Consultant

Gabriel Alejandro Hernández Muñoz is a political scientist with professional experience in evaluating investment projects, programs, and public policies using qualitative approaches, methodologies, and techniques. He has also delved into topics related to peacebuilding from the perspectives of anti-corruption, access to information, and transparency. He has been with Econometría since 2024 as a qualitative analyst, where he is responsible for developing research methodologies, as well as systematizing and analyzing qualitative data.

Vanessa Parada

Consultora de Proyectos

Vanessa Parada Romero es historiadora de la Universidad Nacional de Colombia, especialista en Métodos y Técnicas de Investigación Social por CLACSO y actual candidata a Magíster en Estudios Sociales de la Universidad Pedagógica Nacional. Con trayectoria en Econometría Consultores desde 2020, se ha especializado en la aplicación de metodologías cualitativas para procesos de Monitoreo, Evaluación y Aprendizaje (MEL). Su labor se destaca por la integración de una perspectiva de género transversal en el trabajo con comunidades vulnerables, combinando la rigurosidad de la investigación de archivo con el análisis social aplicado para generar soluciones con enfoque diferencial y basadas en evidencia.

Vanessa Parada

Consultora de Proyectos

Vanessa Parada Romero es historiadora de la Universidad Nacional de Colombia, especialista en Métodos y Técnicas de Investigación Social por CLACSO y actual candidata a Magíster en Estudios Sociales de la Universidad Pedagógica Nacional. Con trayectoria en Econometría Consultores desde 2020, se ha especializado en la aplicación de metodologías cualitativas para procesos de Monitoreo, Evaluación y Aprendizaje (MEL). Su labor se destaca por la integración de una perspectiva de género transversal en el trabajo con comunidades vulnerables, combinando la rigurosidad de la investigación de archivo con el análisis social aplicado para generar soluciones con enfoque diferencial y basadas en evidencia.

Vanessa Parada

Project Consultant

Vanessa Parada Romero is a historian from the National University of Colombia, a specialist in Social Research Methods and Techniques from CLACSO, and is currently pursuing a master’s degree in Social Studies at the National Pedagogical University. Having worked at Econometría Consultores since 2020, she has specialized in the application of qualitative methodologies for Monitoring, Evaluation, and Learning (MEL) processes. Her work stands out for integrating a cross-cutting gender perspective into her work with vulnerable communities, combining the rigor of archival research with applied social analysis to generate evidence-based solutions tailored to specific contexts.

Vanessa Parada

Project Consultant

Vanessa Parada Romero is a historian from the National University of Colombia, a specialist in Social Research Methods and Techniques from CLACSO, and is currently pursuing a master’s degree in Social Studies at the National Pedagogical University. Having worked at Econometría Consultores since 2020, she has specialized in the application of qualitative methodologies for Monitoring, Evaluation, and Learning (MEL) processes. Her work stands out for integrating a cross-cutting gender perspective into her work with vulnerable communities, combining the rigor of archival research with applied social analysis to generate evidence-based solutions tailored to specific contexts.

Julián Monroy

Consultor de Proyectos

Julián David Monroy Calixto es economista con más de cinco años de experiencia laboral. Desde 2024, está vinculado a Econometría S.A.S. como consultor de proyectos. Ha participado en proyectos de consultoría económica y social de alcance nacional e internacional, destacándose en el diseño de instrumentos de recolección de información y datamining. Asimismo, ha contribuido en la organización, procesamiento y análisis de datos, la creación de indicadores mediante el uso de Stata y RStudio, y la redacción de informes técnicos de resultados.

Julián Monroy

Consultor de Proyectos

Julián David Monroy Calixto es economista con más de cinco años de experiencia laboral. Desde 2024, está vinculado a Econometría S.A.S. como consultor de proyectos. Ha participado en proyectos de consultoría económica y social de alcance nacional e internacional, destacándose en el diseño de instrumentos de recolección de información y datamining. Asimismo, ha contribuido en la organización, procesamiento y análisis de datos, la creación de indicadores mediante el uso de Stata y RStudio, y la redacción de informes técnicos de resultados.

Julián Monroy

Project Consultant

Julian David Monroy Calixto is an economist with more than five years of work experience. Since 2024, he has been linked to Econometría S.A.S. as a project consultant. He has participated in economic and social consulting projects of national and international scope, outstandingly contributing to the design of information collection instruments and datamining. Likewise, he has contributed to the organization, processing, and analysis of data, the creation of indicators through the use of Stata and RStudio, and the drafting of technical results reports.

Julián Monroy

Project Consultant

Julián David Monroy Calixto is an economist with more than five years of work experience. Since 2024, he has been linked to Econometría S.A.S. as a project consultant. He has participated in economic and social consulting projects of national and international scope, outstandingly contributing to the design of information collection instruments and datamining. Likewise, he has contributed to the organization, processing, and analysis of data, the creation of indicators through the use of Stata and RStudio, and the drafting of technical results reports.

Jonathan Beltrán

Operative Assistant

Jonathan Sait Beltrán is a Banking and Finance Technician and a Systems Engineering student, with experience in customer service processes and information collection through telephone channels. He has worked as a telephone supervisor at Econometría Consultores, where he coordinated teams of interviewers, monitored information quality, and ensured compliance with productivity standards in data‑collection operations.

He has call‑center experience in organizations such as BBVA, AV Villas, and Konecta, developing skills in database management, user contact, survey administration, issue resolution, and adherence to service protocols. He stands out for his effective communication, service orientation, organization, and teamwork.

His profile is well‑suited to supporting telephone data‑collection processes, ensuring high‑quality data capture, goal achievement, and proper management of respondents.

Jonathan Beltrán

Operative Assistant

Jonathan Sait Beltrán is a Banking and Finance Technician and a Systems Engineering student, with experience in customer service processes and information collection through telephone channels. He has worked as a telephone supervisor at Econometría Consultores, where he coordinated teams of interviewers, monitored information quality, and ensured compliance with productivity standards in data‑collection operations.

He has call‑center experience in organizations such as BBVA, AV Villas, and Konecta, developing skills in database management, user contact, survey administration, issue resolution, and adherence to service protocols. He stands out for his effective communication, service orientation, organization, and teamwork.

His profile is well‑suited to supporting telephone data‑collection processes, ensuring high‑quality data capture, goal achievement, and proper management of respondents.

Jonathan Beltrán

Auxiliar Operativo

Jonathan Sait Beltrán es Técnico en Banca y Finanzas y estudiante de Ingeniería de Sistemas, con experiencia en procesos de atención al cliente y recolección de información mediante canales telefónicos. Ha trabajado como supervisor telefónico en Econometría Consultores, donde ha coordinado equipos de encuestadores, monitoreado la calidad de la información y asegurado el cumplimiento de estándares de productividad en operativos de recolección de datos.

Cuenta con experiencia en call center en entidades como BBVA, AV Villas y Konecta, desarrollando habilidades en manejo de bases de datos, contacto con usuarios, aplicación de encuestas, resolución de inquietudes y seguimiento de protocolos de atención. Se destaca por su capacidad para la comunicación efectiva, orientación al servicio, organización y trabajo en equipo.

Su perfil es idóneo para apoyar procesos de recolección de información telefónica, garantizando calidad en la captura de datos, cumplimiento de metas y adecuado manejo de los informantes.

Jonathan Beltrán

Auxiliar Operativo

Jonathan Sait Beltrán es Técnico en Banca y Finanzas y estudiante de Ingeniería de Sistemas, con experiencia en procesos de atención al cliente y recolección de información mediante canales telefónicos. Ha trabajado como supervisor telefónico en Econometría Consultores, donde ha coordinado equipos de encuestadores, monitoreado la calidad de la información y asegurado el cumplimiento de estándares de productividad en operativos de recolección de datos.

Cuenta con experiencia en call center en entidades como BBVA, AV Villas y Konecta, desarrollando habilidades en manejo de bases de datos, contacto con usuarios, aplicación de encuestas, resolución de inquietudes y seguimiento de protocolos de atención. Se destaca por su capacidad para la comunicación efectiva, orientación al servicio, organización y trabajo en equipo.

Su perfil es idóneo para apoyar procesos de recolección de información telefónica, garantizando calidad en la captura de datos, cumplimiento de metas y adecuado manejo de los informantes.

Leonardo Ambuila

Accountant

Leonardo Ambuila is a Certified Public Accountant and Specialist in Financial Management, with extensive experience in accounting, financial, and tax matters. His career has allowed him to participate in various financial and accounting management processes within organizations, ensuring regulatory compliance and operational efficiency. He has strong skills in developing financial models and controlling cash flow, ensuring the fulfillment of corporate obligations. His interests focus on optimizing financial processes and generating organizational value.

Leonardo Ambuila

Accountant

Leonardo Ambuila is a Certified Public Accountant and Specialist in Financial Management, with extensive experience in accounting, financial, and tax matters. His career has allowed him to participate in various financial and accounting management processes within organizations, ensuring regulatory compliance and operational efficiency. He has strong skills in developing financial models and controlling cash flow, ensuring the fulfillment of corporate obligations. His interests focus on optimizing financial processes and generating organizational value.

Leonardo Ambuila

Contador

Leonardo Ambuila es Contador Público y Especialista en Gerencia Financiera, con amplia experiencia en los ámbitos contable, financiero y tributario. Su trayectoria le ha permitido participar en los diferentes procesos de gestión financiera y contable dentro de las organizaciones, garantizando el cumplimiento normativo y la eficiencia operativa. Cuenta con habilidades en la elaboración de modelos financieros y el control del flujo de caja, asegurando el cumplimiento de las obligaciones empresariales. Sus intereses se enfocan en la optimización de los procesos financieros y la generación de valor organizacional.

Leonardo Ambuila

Contador

Leonardo Ambuila es Contador Público y Especialista en Gerencia Financiera, con amplia experiencia en los ámbitos contable, financiero y tributario. Su trayectoria le ha permitido participar en los diferentes procesos de gestión financiera y contable dentro de las organizaciones, garantizando el cumplimiento normativo y la eficiencia operativa. Cuenta con habilidades en la elaboración de modelos financieros y el control del flujo de caja, asegurando el cumplimiento de las obligaciones empresariales. Sus intereses se enfocan en la optimización de los procesos financieros y la generación de valor organizacional.

Eliana Acevedo

Accounting Assistant

Eliana Acevedo is a Certified Public Accountant and Business Administrator, with a specialization in Tax Management. She is currently pursuing a Master’s degree in Strategic Human Resources Management. She has been working in the accounting field since 2024 and has extensive experience in administrative and coordination processes. Her work focuses on managing accounting and tax processes, promoting regulatory compliance, data accuracy, and continuous improvement. Her professional interests center on integrating accounting, financial, and human resources processes to contribute to more efficient and coordinated organizational management.

Eliana Acevedo

Accounting Assistant

Eliana Acevedo is a Certified Public Accountant and Business Administrator, with a specialization in Tax Management. She is currently pursuing a Master’s degree in Strategic Human Resources Management. She has been working in the accounting field since 2024 and has extensive experience in administrative and coordination processes. Her work focuses on managing accounting and tax processes, promoting regulatory compliance, data accuracy, and continuous improvement. Her professional interests center on integrating accounting, financial, and human resources processes to contribute to more efficient and coordinated organizational management.

Eliana Acevedo

Auxiliar Contable

Eliana Acevedo es Contadora Pública y Administradora de Empresas, con especialización en Gerencia Tributaria. Actualmente cursa una Maestría en Gerencia Estratégica del Talento Humano. Está vinculada al área contable desde el 2024 y cuenta con amplia experiencia en procesos administrativos y de coordinación. Su trabajo se enfoca en la gestión de procesos contables y tributarios, promoviendo el cumplimiento normativo, la precisión de la información y la mejora continua. Sus intereses profesionales se orientan hacia la integración de los procesos contables, financieros y de talento humano, con el propósito de contribuir a una gestión organizacional más eficiente y articulada.

Eliana Acevedo

Auxiliar Contable

Eliana Acevedo es Contadora Pública y Administradora de Empresas, con especialización en Gerencia Tributaria. Actualmente cursa una Maestría en Gerencia Estratégica del Talento Humano. Está vinculada al área contable desde el 2024 y cuenta con amplia experiencia en procesos administrativos y de coordinación. Su trabajo se enfoca en la gestión de procesos contables y tributarios, promoviendo el cumplimiento normativo, la precisión de la información y la mejora continua. Sus intereses profesionales se orientan hacia la integración de los procesos contables, financieros y de talento humano, con el propósito de contribuir a una gestión organizacional más eficiente y articulada.

Julio Gómez

Project Coordinator

Julio Esteban Gómez Arévalo is a Political Science and International Relations Major from the University of Redlands, with a Master’s in Public Policy from the University of Maryland and a specialization in Econometrics from Universidad Externado de Colombia. His expertise lies in designing, implementing, and evaluating public policies using mixed methods, integrating statistical and econometric analysis with qualitative approaches. Skilled in data analysis and programming for evidence-based decision-making.

Julio Gómez

Project Coordinator

Julio Esteban Gómez Arévalo is a Political Science and International Relations Major from the University of Redlands, with a Master’s in Public Policy from the University of Maryland and a specialization in Econometrics from Universidad Externado de Colombia. His expertise lies in designing, implementing, and evaluating public policies using mixed methods, integrating statistical and econometric analysis with qualitative approaches. Skilled in data analysis and programming for evidence-based decision-making.

Julio Gómez

Coordinador de Proyectos

Julio Esteban Gómez Arévalo es politólogo internacionalista de la Universidad de Redlands, con una maestría en Política Pública de la Universidad de Maryland, y una especialización en Econometría de la Universidad Externado de Colombia. Su experiencia se centra en el diseño, implementación y evaluación de políticas públicas con métodos mixtos, combinando estadística y econometría con análisis cualitativo. Especialista en análisis de datos y programación para la toma de decisiones basada en evidencia.

Julio Gómez

Consultor Junior

Julio Esteban Gómez Arévalo es politólogo internacionalista de la Universidad de Redlands, con una maestría en Política Pública de la Universidad de Maryland, y una especialización en Econometría de la Universidad Externado de Colombia. Su experiencia se centra en el diseño, implementación y evaluación de políticas públicas con métodos mixtos, combinando estadística y econometría con análisis cualitativo. Especialista en análisis de datos y programación para la toma de decisiones basada en evidencia.

Daniel López

Project Consultant

Daniel Francisco López Naranjo is a Political Science from the National University of Colombia and a Master’s degree in Administration and Public Policy from the Center for Economic Research and Teaching (CIDE). He has experience in public policy evaluation, project design, applied research, and university teaching. He has served as a consultant for government entities, international organizations, and development agencies, supporting evidence-based decision-making.

Daniel López

Project Consultant

Daniel Francisco López Naranjo is a Political Science from the National University of Colombia and a Master’s degree in Administration and Public Policy from the Center for Economic Research and Teaching (CIDE). He has experience in public policy evaluation, project design, applied research, and university teaching. He has served as a consultant for government entities, international organizations, and development agencies, supporting evidence-based decision-making.

Daniel López

Consultor de Proyectos

Daniel López es Politólogo por la Universidad Nacional de Colombia y Magíster en Administración y Políticas Públicas por el Centro de Investigación y Docencia Económicas (CIDE). Cuenta con experiencia en evaluación de políticas públicas, formulación de proyectos, investigación aplicada y docencia universitaria. Ha participado en consultorías para entidades gubernamentales, organismos internacionales y agencias de cooperación, apoyando la toma de decisiones basada en evidencia.

Daniel López

Consultor de Proyectos

Daniel López es Politólogo por la Universidad Nacional de Colombia y Magíster en Administración y Políticas Públicas por el Centro de Investigación y Docencia Económicas (CIDE). Cuenta con experiencia en evaluación de políticas públicas, formulación de proyectos, investigación aplicada y docencia universitaria. Ha participado en consultorías para entidades gubernamentales, organismos internacionales y agencias de cooperación, apoyando la toma de decisiones basada en evidencia.

Katherinne Alvarado

Fieldwork Manager

Katherinne Alvarado Acevedo is an Industrial Engineer with experience in managing and coordinating quantitative data‑collection processes. She has been part of Econometría since 2019 and has participated in more than 12 consulting projects with the firm. Her main areas of interest include social inclusion, logistics, health, public policies, and territorial, urban, and rural development, among others.

Katherinne Alvarado

Fieldwork Manager

Katherinne Alvarado Acevedo is an Industrial Engineer with experience in managing and coordinating quantitative data‑collection processes. She has been part of Econometría since 2019 and has participated in more than 12 consulting projects with the firm. Her main areas of interest include social inclusion, logistics, health, public policies, and territorial, urban, and rural development, among others.

Katherinne Alvarado

Líder Trabajo de Campo

Katherinne Alvarado Acevedo es Ingeniera Industrial, con experiencia en gestión y coordinación de recolección de datos cuantitativos, se encuentra vinculada a Econometría desde el 2019 y ha participado en más de 12 consultorías con la firma. Sus áreas de interés son principalmente: Inclusión social, logística, salud, políticas públicas, desarrollo territorial, urbano y rural, entre otros.

Katherinne Alvarado

Líder Trabajo de Campo

Katherinne Alvarado Acevedo es Ingeniera Industrial, con experiencia en gestión y coordinación de recolección de datos cuantitativos, se encuentra vinculada a Econometría desde el 2019 y ha participado en más de 12 consultorías con la firma. Sus áreas de interés son principalmente: Inclusión social, logística, salud, políticas públicas, desarrollo territorial, urbano y rural, entre otros.

Santiago Noguera

Project Consultant

Santiago Noguera Cotes studied economics at the Universidad de Los Andes and has been part of the Econometría since 2023. His areas of interest include macroeconomic analysis, impact evaluation, economic development, and the informal economy.

Santiago Noguera

Project Consultant

Santiago Noguera Cotes studied economics at the Universidad de Los Andes and has been part of the Econometría since 2023. His areas of interest include macroeconomic analysis, impact evaluation, economic development, and the informal economy.

Santiago Noguera

Consultor de Proyectos

Santiago Noguera Cotes es economista de la Universidad de los Andes y hace parte del equipo de Econometría desde el año 2023. Sus áreas de interés son el análisis macroeconómico, la evaluación de impacto, el desarrollo económico y la economía informal.

Santiago Noguera

Consultor de Proyectos

Santiago Noguera Cotes es economista de la Universidad de los Andes y hace parte del equipo de Econometría desde el año 2023. Sus áreas de interés son el análisis macroeconómico, la evaluación de impacto, el desarrollo económico y la economía informal.

Diego Sandoval

In memory of

Founder

Diego Sandoval Peralta, industrial engineer, economist and MBA from Universidad de los Andes and M. Phil (cand.) in economics from Oxford University. Until 2016 and for 30 years he was Director of Econometrics. He participated in more than 150 projects as director or expert. His areas of expertise were in economic and financial structuring and evaluation of projects, evaluation of public policies and sectoral analysis in agriculture, transportation and regional development.

Diego Sandoval

In memory of

Founder

Diego Sandoval Peralta, industrial engineer, economist and MBA from Universidad de los Andes and M. Phil (cand.) in economics from Oxford University. Until 2016 and for 30 years he was Director of Econometrics. He participated in more than 150 projects as director or expert. His areas of expertise were in economic and financial structuring and evaluation of projects, evaluation of public policies and sectoral analysis in agriculture, transportation and regional development.

Zuleima Urrea

Data Collection Director

Zuleima Urrea is an agricultural engineer, a graduate of the Universidad Surcolombiana, with a specialization in social management from Uniminuto and a master's degree in project management from EAN University. She has experience in the design, planning, monitoring, and execution of data collection operations at the national level, as well as in the planning, advising, and support of data collection in Central American and Caribbean countries. Her experience includes managing work teams and handling administrative and operational aspects of qualitative and quantitative data collection in urban and rural areas, both in person and virtually. She has participated in projects related to the following themes: education, health, early childhood development, socioeconomics, rural finance, and others.

Zuleima Urrea

Data Collection Director

Zuleima Urrea is an agricultural engineer, a graduate of the Universidad Surcolombiana, with a specialization in social management from Uniminuto and a master's degree in project management from EAN University. She has experience in the design, planning, monitoring, and execution of data collection operations at the national level, as well as in the planning, advising, and support of data collection in Central American and Caribbean countries. Her experience includes managing work teams and handling administrative and operational aspects of qualitative and quantitative data collection in urban and rural areas, both in person and virtually. She has participated in projects related to the following themes: education, health, early childhood development, socioeconomics, rural finance, and others.

Zuleima Urrea

Directora Recolección de Información

Zuleima Urrea es Ingeniera agrícola, egresada de la Universidad Surcolombiana con Especialización en gerencia social de Uniminuto y Maestría en gerencia de proyectos de la EAN. Con experiencia en diseño, planeación, seguimiento y ejecución de operativos de recolección de información a nivel nacional y en la planeación, asesoría y acompañamiento de recolecciones de información en países de Centroamérica y el Caribe. Su experiencia incluye la gestión de equipos de trabajo, el manejo de aspectos administrativos y operativos para recolecciones cualitativas y cuantitativas, en zona urbana y rural, presencial y virtual. Ha participado en proyectos relacionados con las siguientes temáticas: educación, salud, primera infancia, socioeconómicos, finanzas rurales, entre otros.

Zuleima Urrea

Directora Recolección de Información

Zuleima Urrea es Ingeniera agrícola, egresada de la Universidad Surcolombiana con Especialización en gerencia social de Uniminuto y Maestría en gerencia de proyectos de la EAN. Con experiencia en diseño, planeación, seguimiento y ejecución de operativos de recolección de información a nivel nacional y en la planeación, asesoría y acompañamiento de recolecciones de información en países de Centroamérica y el Caribe. Su experiencia incluye la gestión de equipos de trabajo, el manejo de aspectos administrativos y operativos para recolecciones cualitativas y cuantitativas, en zona urbana y rural, presencial y virtual. Ha participado en proyectos relacionados con las siguientes temáticas: educación, salud, primera infancia, socioeconómicos, finanzas rurales, entre otros.

Manuel Herrera

Project Consultant

Manuel Herrera holds a degree in Economics from the Universidad del Rosario and a specialization in Econometrics from the Universidad Externado de Colombia. He has more than 5 years of experience in economic consulting, impact assessment, and quantitative analysis as a consultant at Econometría Consultores.

He has participated in more than 25 projects for national and international organizations such as UNICEF, the IDB, the World Bank, USAID, the WFP, the DNP, the ICBF, and the Bavaria Foundation, covering sectors including education, early childhood, gender, the environment, security, and justice. His key areas of expertise include the design of data collection instruments, the development of indicators and theories of change, impact evaluations, geospatial analysis, and econometric modeling.

For data processing and analysis, he uses R, STATA, QGIS, and Python. He is fluent in English (B2) and is committed to generating rigorous evidence to inform public policy decision-making.

Manuel Herrera

Project Consultant

Manuel Herrera holds a degree in Economics from the Universidad del Rosario and a specialization in Econometrics from the Universidad Externado de Colombia. He has more than 5 years of experience in economic consulting, impact assessment, and quantitative analysis as a consultant at Econometría Consultores.

He has participated in more than 25 projects for national and international organizations such as UNICEF, the IDB, the World Bank, USAID, the WFP, the DNP, the ICBF, and the Bavaria Foundation, covering sectors including education, early childhood, gender, the environment, security, and justice. His key areas of expertise include the design of data collection instruments, the development of indicators and theories of change, impact evaluations, geospatial analysis, and econometric modeling.

For data processing and analysis, he uses R, STATA, QGIS, and Python. He is fluent in English (B2) and is committed to generating rigorous evidence to inform public policy decision-making.

Yaneth Mendoza

General Service Assistant

Yaneth Mendoza has worked for the company for more than 7 years as part of Econometría’s general service team.

Yaneth Mendoza

General Service Assistant

Yaneth Mendoza has worked for the company for more than 7 years as part of Econometría’s general service team.

Maira Quiroz

Financial Coordinator

Maira Quiroz is a Finance professional, specialist in Finance, and holds a Master’s degree in Financial Management from Universidad EAFIT. She has been part of Econometría since 2015 and has experience in managing international operations, treasury, and financial analysis. Her interests focus on the management and optimization of corporate finance; the design of dynamic financial models aligned with the organization’s strategic planning; and transforming financial analysis into a decision‑making tool that provides strategic insight through execution monitoring.

Maira Quiroz

Financial Coordinator

Maira Quiroz is a Finance professional, specialist in Finance, and holds a Master’s degree in Financial Management from Universidad EAFIT. She has been part of Econometría since 2015 and has experience in managing international operations, treasury, and financial analysis. Her interests focus on the management and optimization of corporate finance; the design of dynamic financial models aligned with the organization’s strategic planning; and transforming financial analysis into a decision‑making tool that provides strategic insight through execution monitoring.

July González

Administrative and Financial Assistant

July González is a specialist in occupational risk management, safety, and health. She holds a degree in business administration with a focus on integrated HSEQ management systems and comprehensive project management. She has extensive experience in managing, updating, and monitoring occupational health and safety management systems.

July González

Administrative and Financial Assistant

July González is a specialist in occupational risk management, safety, and health. She holds a degree in business administration with a focus on integrated HSEQ management systems and comprehensive project management. She has extensive experience in managing, updating, and monitoring occupational health and safety management systems.

Joe Andres Gonzalez

Courier

Joe Andrés Gonzalez Vásquez is a motorcycle maintenance and repair technician. He has been with Econometría since 2012 as a messenger in the administrative department.

Joe Andres Gonzalez

Courier

Joe Andrés Gonzalez Vásquez is a motorcycle maintenance and repair technician. He has been with Econometría since 2012 as a messenger in the administrative department.

Ana Rosa Ortigoza

Editing Assistant

Ana Rosa Ortigoza Verdu is an assistant accounting secretary with more than 20 years of experience in the field. She has worked with Econometría since 2012 and has participated in proposals for different private and public entities, as well as in editing of reports on projects, from income to current affairs.

Ana Rosa Ortigoza

Editing Assistant

Ana Rosa Ortigoza Verdu is an assistant accounting secretary with more than 20 years of experience in the field. She has worked with Econometría since 2012 and has participated in proposals for different private and public entities, as well as in editing of reports on projects, from income to current affairs.

Ana María Sandoval

Communications Analyst

Ana María Sandoval is a Digital Graphic Designer with more than 5 years of work experience in the field. She has been linked to Econometría since 2020, first as an apprentice from the SENA and then as a Communications Analyst during the same year. Currently, she is in charge of the company's internal and external communications, social networks, content management for the website, design and development of pieces in projects, and management of the firm's visual identity.

Ana María Sandoval

Communications Analyst

Ana María Sandoval is a Digital Graphic Designer with more than 5 years of work experience in the field. She has been linked to Econometría since 2020, first as an apprentice from the SENA and then as a Communications Analyst during the same year. Currently, she is in charge of the company's internal and external communications, social networks, content management for the website, design and development of pieces in projects, and management of the firm's visual identity.

Yeimy Sandoval

Administrative Assistant

Yeimy Sandoval Olaya is an expert in psychology and has held links with the organization since 2016. She has participated in more than 20 consultancies over this period, with principal areas of interest in: Human rights, social inclusion, vulnerable populations, education, and social protection.

She has professional experience in coordination of qualitative data collection, both in person and online, in which she has overseen fieldwork teams delivering interviews, focus groups and telephone surveys. She has overseen telephone surveys as a quality coordinator; and she has also provided a broad range of transversal support to information-gathering studies, from delivering transcriptions to coordinating a group of transcribers by carrying out quality controls of their work.

Yeimy Sandoval

Administrative Assistant

Yeimy Sandoval Olaya is an expert in psychology and has held links with the organization since 2016. She has participated in more than 20 consultancies over this period, with principal areas of interest in: Human rights, social inclusion, vulnerable populations, education, and social protection.

She has professional experience in coordination of qualitative data collection, both in person and online, in which she has overseen fieldwork teams delivering interviews, focus groups and telephone surveys. She has overseen telephone surveys as a quality coordinator; and she has also provided a broad range of transversal support to information-gathering studies, from delivering transcriptions to coordinating a group of transcribers by carrying out quality controls of their work.

Jorge Andrés Moreno

Fieldwork Manager

Jorge Andrés Moreno is currently pursuing studies in agricultural business administration and has more than 18 years of experience in data collection. He has worked with Econometría since 2014, participating in more than 30 consultancies as coordinator of quantitative and qualitative data collection. His principal areas of interest are mainly in projects: Socioeconomic, Agricultural, Business, Health and Education, among others.

Jorge Andrés Moreno

Fieldwork Manager

Jorge Andrés Moreno is currently pursuing studies in agricultural business administration and has more than 18 years of experience in data collection. He has worked with Econometría since 2014, participating in more than 30 consultancies as coordinator of quantitative and qualitative data collection. His principal areas of interest are mainly in projects: Socioeconomic, Agricultural, Business, Health and Education, among others.

Ilber Arnoby Iter

Operative Assistant

Ilber Iter Guainas holds a degree in Business Management and a certificate in Administrative Assistance, and has completed two semesters of public accounting. He has been with Econometría since 2017, supporting the finance and administration departments. He currently works on various activities related to the research and evaluation projects carried out by the company. He also has extensive experience in accounting and in managing support for project execution, as well as experience in customer service, protocol, and logistics.

Ilber Arnoby Iter

Operative Assistant

Ilber Iter Guainas holds a degree in Business Management and a certificate in Administrative Assistance, and has completed two semesters of public accounting. He has been with Econometría since 2017, supporting the finance and administration departments. He currently works on various activities related to the research and evaluation projects carried out by the company. He also has extensive experience in accounting and in managing support for project execution, as well as experience in customer service, protocol, and logistics.

Edith Machado

Fieldwork Manager